BOND YIELDS EXPLODE HIGHER ON HOT ADP, ISM & US$ - ALL EYES ON OCTOBER NFP REPORT

KEY POINTS

- On Wednesday, bonds were routed and the selloff was the talk of the financial universe.

- 30-year and 10-year yields hit their highest levels since 2014 and 2011, respectively.

- Understanding why is critical, as is appreciating the extent to which Friday's jobs report just became even more critical than it already was.

Here's everything you need to know.

A couple of weeks back, I wrote something for this platform called "The Bond Selloff That Nobody Noticed".

That was a recap of events that transpired during the week of September 17, when yields rose on what looked like a combination of rising inflation expectations and the term premium trade.

One of the oddities of that week was the dollar (NYSEARCA:UUP), which did not rise in tandem with U.S. yields. Instead, the greenback fell as commodities rallied, a combination that helped buoy sentiment in downtrodden ex-U.S. assets, particularly emerging markets, where equities outperformed their U.S. counterparts handily and currencies logged their best week since February.

On September 18, Jeff Gundlach expressed his incredulity at the perceived lack of press coverage:

Fast forward to Wednesday and Treasurys sold off hard. This time around, the financial media definitely took note.

Wednesday's bond rout was the talk of the financial universe as 30-year and 10-year yields hit their highest levels since 2014 and 2011, respectively.

(Bloomberg)

(Bloomberg)

The selloff began in earnest with a big ADP beat and gathered steam following an extremely hot ISM services print.

(Bloomberg)

Futures volume was enormous (around 180% of the 10-day average) and the close was very ugly, with 10-year yields rising further and closing near the day highs:

(Bloomberg)

The curve bear steepened, as the 2s10s sliced up through 30bps, the widest in at least two months:

(Bloomberg)

What should you make of all this?

Well, first of all, based on the volume, it looks like folks got stopped out, which likely exacerbated the selloff. Either that, or people were adding new shorts. If it's the latter, just note that the spec short in the 10-year was already sitting at a record high (this the latest data available, current through Tuesday, September 25):

(Bloomberg)

(Bloomberg)

But more importantly for average investors, this feels a whole lot like late January/early February. We're staring down an acute selloff in bonds that so far has been accompanied by rising stock prices (SPY) and we're headed into a pivotal jobs report on Friday.

In the interest of brevity, I won't recount the whole story here, but do recall that on January 29, I published a post on this platform called "Hey Guys? The Bond Selloff Needs To Stop, Like Right Now". The gist of that piece was that bond yields were rising too far, too fast, and I suggested it was just a matter of time before the stock-bond return correlation flipped positive, leading to a selloff in both equities and bonds at the same time.

Five days later, wage growth came in ahead of expectations and the bottom fell out, as the bond selloff that had been gathering steam for weeks collided with the first real evidence that inflation pressures were starting to build in the U.S. economy.

January was defined by rising yields and a melt-up in U.S. stocks. Incoming Fed Chair Jerome Powell was expected to adopt a more data-dependent approach to monetary policy than his predecessor, and that had markets on edge about inflation.

That is very similar to the current setup. 10-year yields have risen more than 30bps since September 1. Meanwhile, U.S. equities have made new high after new high since August, when the S&P finally recouped losses incurred in February and March.

At the same time, Jerome Powell has repeatedly emphasized how well the U.S. economy is doing and in a speech in Boston on Tuesday, he literally said thisabout the Phillips curve:

I do not see it as likely that the Phillips curve is dead, or that it will soon exact revenge.

You can read the full text of his speech in that linked post, but suffice to say he is playing down the possibility that at some point in this late-stage expansion, wage growth is going to take off and catch the Fed woefully behind the curve.

Today looked like the market attempting not only to catch up to the 2019 dots, but also to start pondering the possibility that inflation could accelerate meaningfully going forward. Consider this out Wednesday morning from Nomura's Charlie McElligott:

I continue to believe that the market’s skepticism on “higher inflation” to be a mis-priced risk that could further escalate the Rates selloff in unruly fashion, especially with the 1) “wage growth” story picking-up further yesterday (Amazon minimum wage hike), 2) four year highs in Crude, 3) the cycle-lows in U-Rate / another large “Labor” beat with ADPs today 4) cycle-highs in Consumer Confidence, 5) 17 year highs in JOLTS Quit Rate…all into the “real-time” escalation of the “QE to QT impulse” broad “bearish fixed-income” catalyst.

That is a characteristically incisive assessment from Charlie.

Again, do note that all of the above raises the stakes for Friday's September jobs report. Nomura reinforced that in a note out Wednesday the gist of which was that payrolls may have an outsized impact given the Fed's data-dependent lean.

The most critical thing to understand about Wednesday is that the market’s interpretation of rising yields can turn on a dime, and this has all the trappings of an inflation scare.

When it comes to rate rise, it’s the “why?” and the “how quickly?” that matter and while the answer to the first question bodes well for risk, we might soon be answering the second question with this: “Too fast”. That is precisely what happened in February. Yields had been rising for quite a while, but stocks took it in stride as the bond selloff was generally seen as a reflection of U.S. economic strength. Finally, there was a tipping point and inflation worries took over.

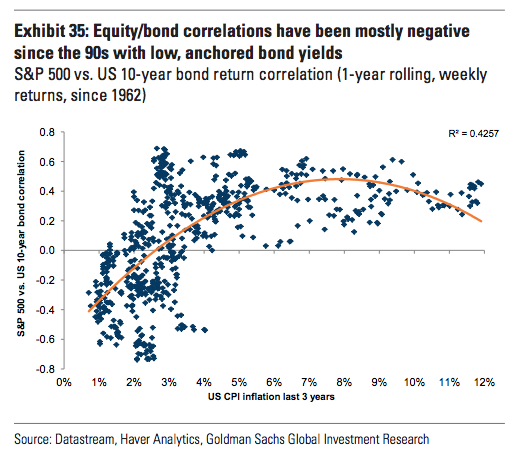

Goldman was out a couple of weeks back reiterating the very same warning they delivered in and around the February selloff - namely that if yields rise by more than two standard deviations in a 3-month period, the 3-month stock-bond return correlation tends to flip positive or, more simply, stocks begin to selloff with bonds.

(Goldman)

(Goldman)

That's the dreaded "diversification desperation" and it plays havoc with balanced portfolios and risk parity. Not to put too fine a point on it, but we're due for drawdown there. In fact, the current bull market in balanced equity/bond portfolios is the longest in history.

(Goldman)

(Goldman)

Here's a bit more from a sweeping new Goldman note that documents the history of balanced portfolios and how the stock-bond correlation has evolved over the years:

While not our base case, with high and rising inflation, like the 70s and 80s, equity/bond correlations turn positive - from US CPI levels above 2% over a 3-year rolling period there have been many instances when equity/bond correlations turned positive (Exhibit 35). Also, the relationship does not appear to be linear - when positive inflation surprises become a bigger worry than negative ones, bonds are unlikely to be good diversifiers for equities and higher yields can weigh on equities.

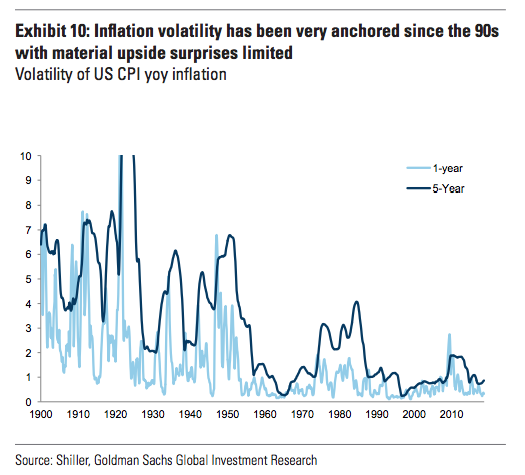

In the same note, Goldman writes that investors may be underestimating the risk of upside surprises in inflation. Here's one more excerpt along with a visual that shows you how well-behaved inflation data has become:

US inflation risk might be higher than investors think. There is always risk of a fast pick of inflation and upward pressure on rates when moving late cycle, especially with US fiscal stimulus and the introduction of trade tariffs. Our economists highlighted capacity constraints and the risk of overheating of the labour market - the current policy backdrop is similar to the runup to the late 60s inflation shock.

You should also be acutely aware of the fact that real yields are to a certain extent a function of inflation expectations given the data-dependent Fed. The more inflation pressure, the more inclined the market believes the Powell Fed will be to respond. A hawkish response pushes real rates higher.

Let me drive that point home in the most poignant way possible. Did you happen to notice when stocks ran out of steam on Wednesday? It was at the precise (almost) moment when 10-year real yields hit 1%:

(Bloomberg)

Nothing further.