THE HEADLINE: The Challenge For Deutsche Bank - Cost-Cutting & Capital-Deployment Conundra

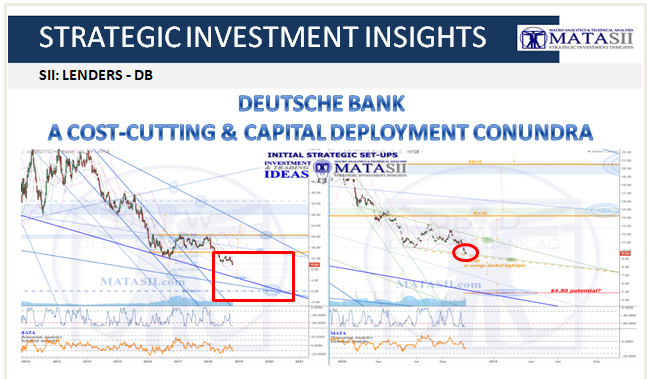

MATASII SII ANALYSIS: DB Deutsche Bank IDEA: October 29th, 2018: Our original IDEA and post for DB was over 2 years ago on June 23rd, 2016; the technicals given then were followed nicely and continue to be respected. The $14.20 level continues to be significant, only now we are looking at it as resistance and a potential long trigger.

The weekly chart (left) shows a large contacting wedge pattern, where the last bounce from the supporting trend line only had the market reach about 1/2 way up inside the wedge, as opposed to having it lift to touch the opposite resistance line of the pattern. Resistance held at $20.50 (given June,2016), the market fell through our original trigger consideration at $14.20, and currently sits at $9.64. Although our original trigger consideration has been moved through, we can still take advantage of more potential down (or up) by continuing to follow the technicals.

The daily chart (right) gives us a closer perspective of the current market and more technicals for consideration. The more recent action from the down has formed a contracting wedge, bound by the green (daily) technicals. An orange dashed highlight marks the daily support and offers a potential trigger consideration if moved over. $9.40 marks the current location, however this could be lower if the support breaks further on. Expect market reaction around the $8.00 level with a potential to reach $4.80 (or lower?).

IF the market finds support and starts to lift, we can also follow it from one technical to the next as it rises. Initially we would like to see at least a move up out of the top of the green daily wedge, however resistance could then potentially be seen around $12.75-$13.00: waiting for the $14.20 level to be broken back over again would offer less risk.

In general we have a negative bias on Lenders, and we are watching to see if this market will again move back to the lower support of the large weekly contracting wedge pattern. Note that if this does happen, there is also a potential for the market to then lift very quickly or "bounce" off the bottom support of the pattern. As the price decreases the risk increases that "something" will occur that could violently reverse the trend. That "something" could be a many number of things, but regardless, it can usually be seen to "coincidentally" occur at the same time the market has reached significant technicals. We'll have to watch and see what happens!

When we first heard news reports about a new investor in Deutsche Bank (DB), we of course assumed that this meant the The Challenge For Deutsche Bank - Cost-Cutting & Capital-Deployment Conundra purchase of new shares and thus an increase in capital. But no, it was merely an “activist investor” taking a stake in existing shares. Is this really news or merely a sign of a top in large bank stocks? The DB common is trading a hair over $10 or just 0.3x book value and has a beta of 1.5.

Douglas Braunstein, founder and managing partner of Hudson Executive Capital and J.P. Morgan's (JPM) former CFO, said in an interview with CNBC that the firm has taken on the stake over the last few months after studying the stock for a year. We’ve been following DB for a lot longer than that and have great difficulty constructing a bull case for the name. But let’s take a look anyway.

First on the list of concerns is profitability. DB has been struggling for years to find a business strategy to deliver consistent profitability, the key measure of stability for any bank. Through the first nine months of the year, DB delivered net income of less than a €1 billion compared with €1.6 billion a year ago. For the full year 2017 the bank lost €750 million. As yet, no one on the management team – if we may so dignify DB’s executives – have been able to articulate a coherent plan to move forward.

Second is capital. DB has just €61 billion or 4% capital to total assets of €1.5 trillion, one of the lowest simple leverage ratios of any major bank worldwide. The bank tries to hide this capital deficiency behind calculations that exclusively use “risk weighted “assets” of just €354 billion. In the bank’s non-GAPP disclosure, there is just €54 billion in tangible capital disclosed for a leverage ratio closer to 3%.

In the Q3 ’18 earnings call, when CEO Christian Sewing said that “we committed to conservative balance sheet management and maintaining a CET1 ratio above 13%,” he was referring to risk weighted assets, not total assets. If one assumes that the entire Basel III/IV framework is a confused mess when it comes to describing risk, then the leverage ratio is what matters. Risk weighted assets is a way to pretend that the rest of the banks in Europe and Asia are solvent.

To be fair to DB, most European banks play the game of only referring to “risk weighted assets” in their financial disclosure to investors. The EU bank regulators are entirely complicit in this charade. Indeed, since the end of 2017 DB’s total capital has actually fallen 4%.

The last major infusion of capital for DB came from the generous folks at HNA, who are in the process of liquidating their debt financed empire at the behest of Uncle Xi. Regulators in the EU and US never asked about the source of the funds provided by HNA nor the beneficial ownership of the Chinese firm. Since the initial investment was raised to almost a 10% stake in 2017, HNA has been a distressed seller, partly because so much of the investment seems to have been funded with debt.

The third key concern among a far longer list of questions is the franchise. The DB supervisory board has shown no vision when it comes to focusing the bank’s business on more profitable areas. DB is more a securities firm than a bank. It does not have a strong banking franchise in Europe and has a mediocre investment banking and capital markets business in London and New York. Ranking eighth in the league tables after Barclays (BCS) and above Wells Fargo & Co. (WFC) in total deals YTD, there is no sector where DB has a commanding presence in either capital markets or investment banking.

Like JPMorgan (JPM) and Citigroup (C), less than a third of DB’s book is allocated to loans, reflecting the bank’s focus on trading and derivatives. The bank does have a strong position in commercial real estate in the US, but the greatly stretched valuations in that sector do not inspire confidence about future loan and securitization volumes. Notice, for example, that the bid for agency RMBS had largely disappeared in the US. Spreads are set to widen as the year-end approaches.

Sewing says that “Our principal near-term target is to reach a return on tangible equity of more than 4% next year.” Such a goal is relatively bold given the parlous state of the banking industry in Europe, but DB’s US peers have equity returns well in excess of twice this level.

Perhaps more frightening is Sewing’s intention to “deploy part of our capital into our business,“ something that DB has never done well. The ill-fated investment in the Postbank, for example, is currently being restructured at a cost of tens of millions of euros as the bank seeks savings by merging the two entities.

So will DB have a negative surprise for investors in Q4’18? As Sewing said during the conference call: “I'm well aware of Deutsche Bank's history of negative surprises in the fourth quarter, and we are absolutely determined to not repeat this.” But even without any drama, the fact remains that cost cutting of various types is the predominant activity at DB this year and in 2019.

Investors can expect another couple hundred million in restructuring charges in the fourth quarter, although DB management is telling investors that overall charges could be well below original estimates for 2018. But the big challenge will be increasing revenue through the enterprise, for example by moving several hundred billion euros earning negative 40bp at the Bundesbank into other, more remunerative activities.

DB executives point to such accomplishments as taking share in the market for leveraged loans, a sector we can be pretty sure will figure prominently in the next downturn in the credit cycle. Despite the happy talk coming from senior management about deploying capital prudently, the fact is that DB does not have a lot of options when it comes to new business outside of a low-quality capital markets business.

Putting scarce capital into growing market share in leveraged loans and collateralized loan obligations (CLOs), for example, strikes us a distinctly unattractive right now. But the fact is that for the past decade or more, DB has made a living of sorts by structuring crappy assets that other banks will not touch. The legal and reputational risk from these activities have been enormous. As CEO Sewing told investors: “[w]e are seen as one of the better banks in this business and, therefore, we see increasing volume.” Wunderbar!