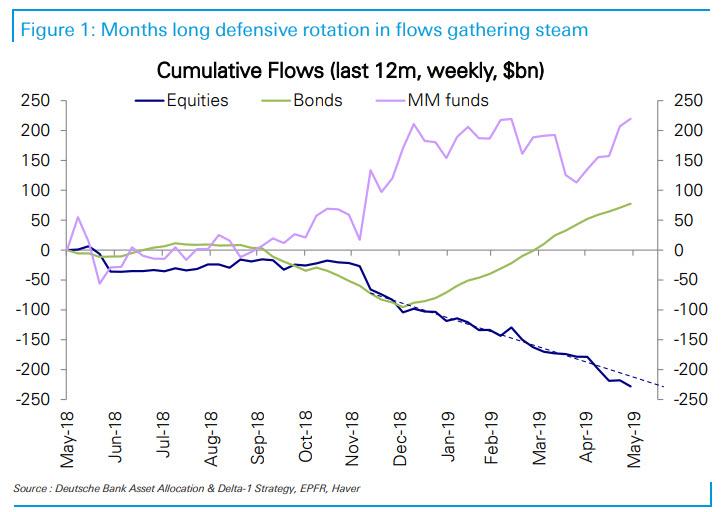

Institutions are shifting in a massive way to Bonds and Money Market Funds as Equity Outflows over the last 6 months have been of historic and and unprecedented levels.

- The S&P has just suffered its third worst month since the US AAA- rating downgrade in August 2011,

- Its worst May in decades,

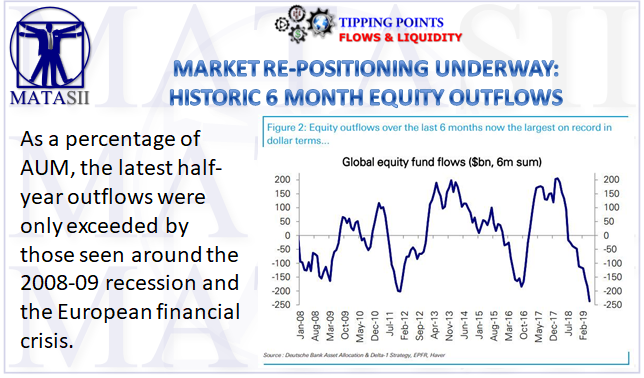

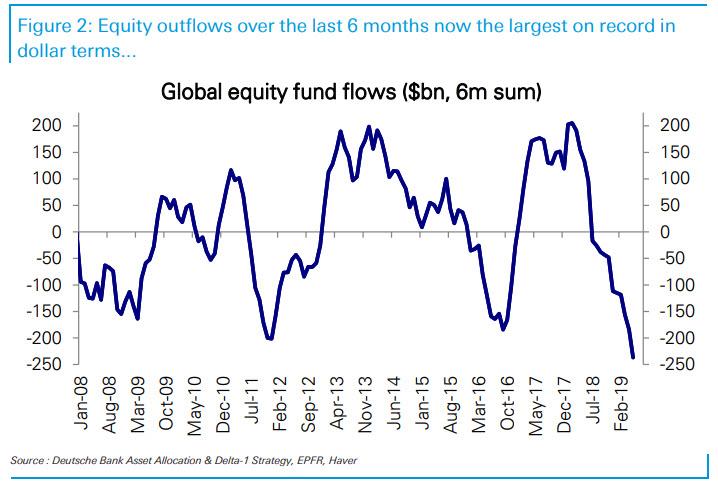

- As a percentage of AUM, the latest half-year outflows were only exceeded by those seen around the 2008-09 recession and the European financial crisis.

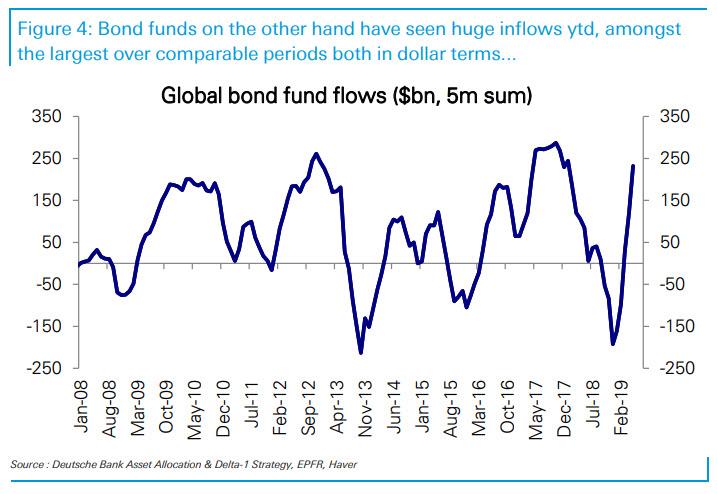

- Bond funds have seen inflows of $220bn ytd

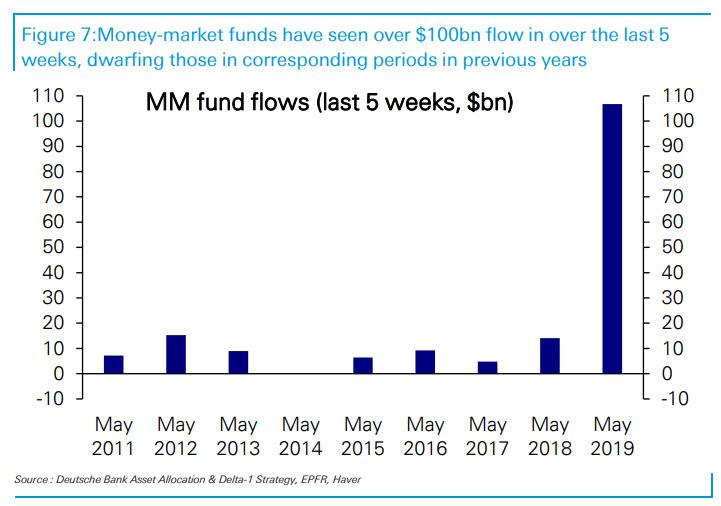

- Money-market funds have seen inflows of over $107bn just in the last 5 weeks, in what is usually a seasonally weak period.

Tyler Durden recaps the flows with supporting charts from Deutsche Bank:

WHERE WE STAND

According to Deutsche Bank, looking at the latest EPFT data, last week the safety bid in flows continued - as one would predict - with large outflows from equity (-$10bn) and HY (-$3bn) funds, but inflows to other bond (+$10bn) and money-market funds (+$12.9bn).

And here, a shocker: equity funds have now seen outflows of -$132bn YTD and -$237bn since December. This means that outflows over the last 6 months in dollar terms have now been larger than over any prior 6-month period.

As a percentage of AUM, the latest half-year outflows were only exceeded by those seen around the 2008-09 recession and the European financial crisis.

Breaking down the flows geographically: the US saw -$8.4bn in outflows, Europe -$1.8bn and Asia ex Japan -$1.7b), while Japan attracted $1.9b in inflows. Broad-based global funds (-$0.3b), global EM funds (-$0.1b) and Latam (-$0.1b), too, saw outflows although at moderate pace. European equity outflows were at their slowest pace in 16 weeks, and were driven both by domestic (-$1.3b) and foreign (-$0.5b) flows. In Japan, on the other hand, domestic investors pumped in $2.4b, while foreign investors pulled out -$0.4b. China funds saw outflows continue (-$1.7b) as it continues to bear the brunt of trade concerns, while India funds got their biggest inflows ($0.3b) since early 2018 after the election results showed a strong renewed mandate for the incumbent administration.

By contrast, bond funds have seen inflows of $220bn ytd...

... close to the largest on record over comparable periods in the past, and money-market funds have seen inflows of over $107bn just in the last 5 weeks, in what is usually a seasonally weak period.

And, as Deutsche Bank confirms what we have been saying through this entire rally, "With trade tensions ratcheting higher yesterday we are likely to see the safety bid strengthen further."

So now that the selling avalanche is now just a matter of when, not if, Deutsche Bank provides some observations on which will be the first investor classes to capitulate:

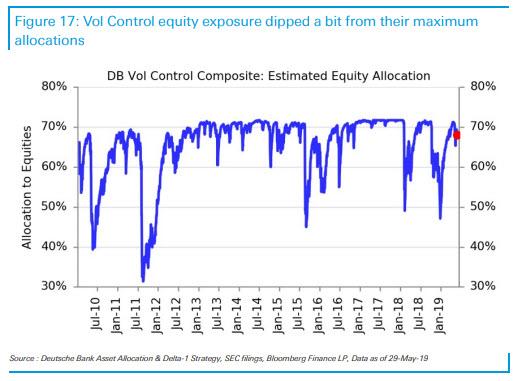

- Vol Control funds will remain sellers as vol rises on the latest selloff. Since the end of April, Vol Control funds have sold net $13-$15bn in equity exposure and if the S&P 500 were to sell-off an additional -2% on Monday, they would have another modest $5-7bn to sell. And since allocations still remain on the higher side, DB warns that the risk is asymmetric to the downside.

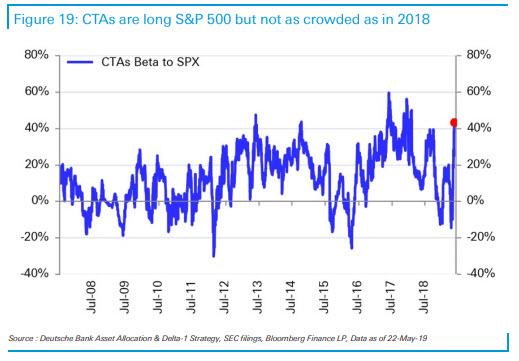

- CTAs also have begun selling as near-term triggers are hit. According to DB, the CTA complex is net long S&P 500, but with lighter positioning versus 2018 sell-offs. Additional selling likely if short-term MAs cross long-term MAs, which requires spot to stay low for the next few weeks.

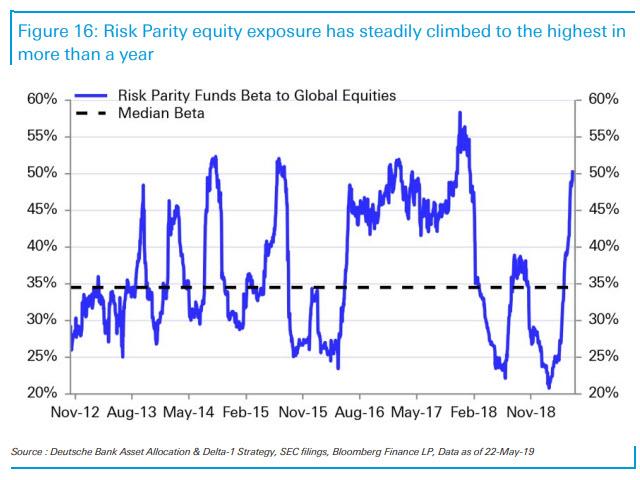

- Risk Parity funds have mostly not reacted to the sell-off yet - as thesestrategies are slow moving - but do have significant beta to the S&P 500. It is possible that some PMs with more discretion de-risked, but most have significant beta to the S&P 500... right as the sell-off is hitting. With 1M vol of the cross asset portfolio only at 5, the negative correlation between equities and bonds continues to offset some of the pick-up in equity volatility

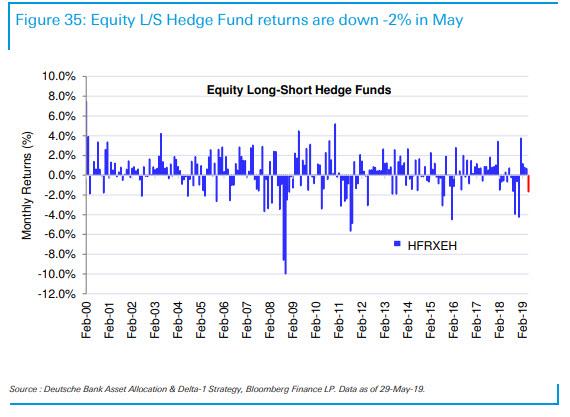

- Away from systematic funds, traditional equity L/S is only down -2% in May...

- ... with low net and gross exposure going into this sell-off (once again, not many appear to have listened to the JPMorgan quant). YTD returns are +4.9%, off from a high of +7%.

- Popular single-stock longs have performed in-line with popular single-stock shorts, while the recent Momentum rally has not significantly impacted returns given the Hedge Fund complex’s relatively flat exposure to the factor.

So as the equity outflows continue, it appears that all those who were betting that longs on the fence and who would be forced to jump in kicking and screaming, were wrong. The only question now is how much of a drop is expected before we finally do see some inflows.... unless of course, there is no catalyst that can take place to change the current status quo - and with both the Fed's reversal and China's record credit injection now in the rearview mirror, one wonders just what will prompt a turnaround to the fund flow direction - in which case global capital markets are about to face a historic day of reckoning.

[SITE INDEX -- TIPPING POINTS - GLOBAL GOVERNANCE FAILURE]

A PUBLIC SOURCED ARTICLE FOR MATASII

READERS REFERENCE: (SUBSCRIBERS & PUBLIC ACCESS)

MATASII RESEARCH ANALYSIS & SYNTHESIS WAS SOURCED FROM:

SOURCE: 06-02-19 - - "Capitulation: Equity Outflows In The Past 6 Months Are Now The Biggest Ever"

FAIR USE NOTICE This site contains copyrighted material the use of which has not always been specifically authorized by the copyright owner. We are making such material available in our efforts to advance understanding of environmental, political, human rights, economic, democracy, scientific, and social justice issues, etc. We believe this constitutes a 'fair use' of any such copyrighted material as provided for in section 107 of the US Copyright Law. In accordance with Title 17 U.S.C. Section 107, the material on this site is distributed without profit to those who have expressed a prior interest in receiving the included information for research and educational purposes. If you wish to use copyrighted material from this site for purposes of your own that go beyond 'fair use', you must obtain permission from the copyright owner.

NOTICE Information on these pages contains forward-looking statements that involve risks and uncertainties. Markets and instruments profiled on this page are for informational purposes only and should not in any way come across as a recommendation to buy or sell in these assets. You should do your own thorough research before making any investment decisions. MATASII.com does not in any way guarantee that this information is free from mistakes, errors, or material misstatements. It also does not guarantee that this information is of a timely nature. Investing in Open Markets involves a great deal of risk, including the loss of all or a portion of your investment, as well as emotional distress. All risks, losses and costs associated with investing, including total loss of principal, are your responsibility.