MONETARY MALPRACTICE: THE PROOF IS NOW EVERYWHERE!

MATASII RESEARCH ANALYSIS & SYNTHESIS:

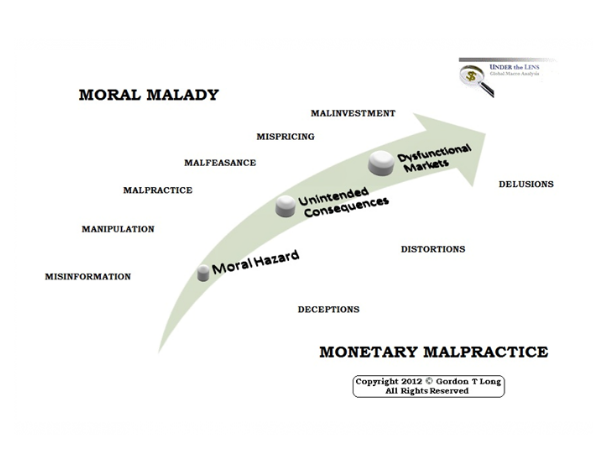

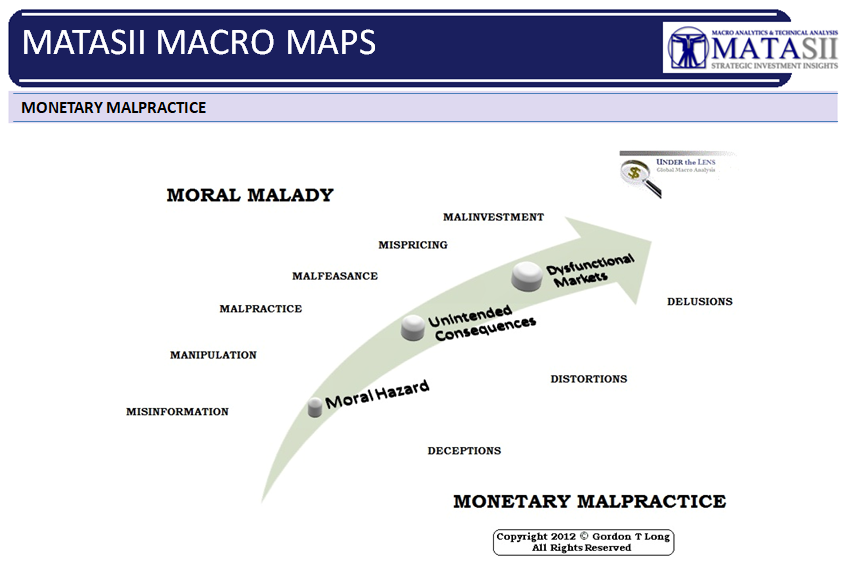

I put this road-map together in 2012 (see copyright logo) on what we should expect based on the Federal Reserve practicing policies of ZIRP and what was then a new concept - Quantitative Easing (QE1). It has proven to be prescient!

Below is a long article by John Mauldin who I have interviewed for the Financial Repression Authority in 2015. I recommend you read it with a clear framework from the context of the following key points which I have pointed out many time since the publication of the road-map.

CAPITALISM REQUIRES:

- COMPETITION: The fostering and rewarding of Winners & Losers,

- CREATIVE DESTRUCTION: So Winners will secure 'scarce' Financing and not the losers (called Zombies & Unicorns in the article below) which survive on 'easy' financing.

- OPEN PRICE DISCOVERY: Prices must trade freely or Price Discovery cannot occur and distortions emerge impacting decision making and creating malinvestment,

- FREE PRICING OF RISK: Must trade freely.

IMPEDIMENTS TO CAPITALISM

- SCALE: Which Stifles & Smothers Innovation

- MANIPULATION: Governments & Central Banks can Distort Reality

- CRONY CAPITALISM: Where "Regulatory Arbitrage" becomes a competitive weapon.

Capitalism is not failing but rather it is our inability to allow it to work and to refrain from manipulating it for expedient political reasons. Since we have failed to steward this properly (at least since the 2008 Financial Crisis) we can expect the following:

WHAT TO EXPECT IN THE 20'S

- Getting Less for More (versus More for Less in a properly function capitalist economy),

- The continuing "Japanization" of the US Economy,

- The next recession will be deeper, longer and far more painful to many more people than your average recession, and could persist as long as the last one:

- GLOBAL: That is because the next recession in all likelihood will be truly global.

- RESPONSE: It will be the response to the last recession that makes the next one so much worse.

- PASSIVE INVESTING: The massive move into low-fee index investing instead of active management will make the next recession more painful.

- Public pensions, are heavily weighted to a form of index investing.

- Public pensions are already significantly underfunded (in general) and a bear market will make them even more so

[SITE INDEX -- MACRO: US - MONETARY POLICY]

A PUBLIC SOURCED ARTICLE FOR MATASII

READERS REFERENCE (SUBSCRIBERS-RESEARCH & PUBLIC ACCESS )

MACRO: US - MONETARY POLICY

SOURCE: 04-10-19 - John Mauldin via MauldinEconomics.com - "The Fed Has Created An Economy Of Zombies And Unicorns"

FAIR USE NOTICE This site contains copyrighted material the use of which has not always been specifically authorized by the copyright owner. We are making such material available in our efforts to advance understanding of environmental, political, human rights, economic, democracy, scientific, and social justice issues, etc. We believe this constitutes a 'fair use' of any such copyrighted material as provided for in section 107 of the US Copyright Law. In accordance with Title 17 U.S.C. Section 107, the material on this site is distributed without profit to those who have expressed a prior interest in receiving the included information for research and educational purposes. If you wish to use copyrighted material from this site for purposes of your own that go beyond 'fair use', you must obtain permission from the copyright owner.

Recession is coming. We can debate the timing, but the economy will turn decisively downward at some point. My own analysis, looking at the data available on April 4, says recession isn’t likely this year but unfortunately looks very probable in 2020.

In addition to when it will happen, there’s also the question of how deep the next recession will be. A shallow downturn wouldn’t be fun, but compared to the last one might feel relatively refreshing.

Alas, I don’t think we will be that lucky. I think the opposite: The next recession will be deeper, longer and far more painful to many more people than your average recession, and could persist as long as the last one. That is because the next recession in all likelihood will be truly global. If you sailed through 2007–2009 without your lifestyle changing, I wouldn’t assume it will happen that way again.

Ironically, but not surprisingly, it will be the response to the last recession that makes the next one so much worse. Part of the reason is that investors once again “learned” that if you simply stay the course, the market will get you back to where you were and more. The massive move into low-fee index investing instead of active management will make the next recession more painful.

You must understand that 75% of today’s wealth is in the hands of retirees and pre-retirees. Most have a significant portion of their money in index funds, and they’re going to see significant erosion of their retirement assets. I’m thinking especially of those depending on public pensions, which are heavily weighted to a form of index investing. Public pensions are already significantly underfunded (in general) and a bear market will make them even more so. It will be painful and I can assure you it will cause a lot of political angst. Today I’ll tell you why I think this. It may be one of the more important letters I’ve written in the recent past, so read carefully.

Central bankers have a well-worn playbook for handling recessions. Cut interest rates, increase liquidity, and otherwise make more capital available to the private sector. This helps businesses hire more workers and raise wages. Then gradually remove all the stimulus as growth recovers. (Usually, at least. Greenspan waited too long to tighten after the 2001 recession and begin raising rates, creating the dynamics for the subprime crisis.)

The playbook truly fell apart in 2008. The system had so much debt that adding yet more of it didn’t have the desired effect. As noted, easy money from the last crisis had created the situation. Even dropping short-term rates to effectively zero didn’t help because it was creditworthiness, not interest costs, that kept people and businesses from borrowing.

The Bernanke Fed’s answer was quantitative easing—essentially a way to stimulate lending at longer maturities. It had an effect but not the intended one. Instead of going to productive use, the new stimulus helped banks deleverage and public companies leverage up and repurchase their own shares, or as we will discuss below, simply buy their competition and short-circuit the “creative destruction” cycle. This pushed asset prices, i.e. the stock market, higher and made it appear recovery was underway. Unfortunately, the “recovery” was the slowest recovery on record.

All that cash eventually trickled through the economy, not to people who would spend it on useful goods and services, but to yield-starved investors. Why were they starving? Because the Fed was keeping rates low. They had little choice but to take more risk, which is what the Fed wanted them to do in the first place. So they plunged money into venture capital, private equity, IPOs, emerging markets, and everything else they could find with potentially decent capital gains and/or yields.

The result was a massive wave of investment, some good and some, well, let’s just say based on hope and little else. And as we know, hope is not a solid investment strategy. Some businesses that had good stories (the so-called unicorns) found themselves covered with cash by investors for whom hope sprang eternal. Eager to show they could turn the cash into gold, the companies sought to emulate the Amazon model, using money to buy growth without profit. In the hopes of going public at some point and cashing in, they kept the game alive. Think Lyft. (Note: I like Lyft and wish them nothing but success. But still…) Investors, because they wanted to believe the story they were investing in was true, watched and waited.

They’re still waiting. And here we are.

Back in November 2018 (which now seems like about 30 years ago) I wrote about a Bank for International Settlements study of “zombie” businesses. Looking at the 32,000 publicly-traded companies in 14 advanced economies, they found 12% were both

- At least 10 years old, and

- Had an interest coverage ratio below 1.0 for three consecutive years.

In other words, these companies weren’t making enough revenue to pay back their loans, much less cover their other expenses and earn a profit.

Note, these were not startup companies. All were at least 10 years old and still in business despite their inability to make any money. Here was my conclusion at the time.

Faced with a probable loss, lenders always face a temptation to “extend and pretend.” They convince themselves that another year or another quarter will let it turn into a sterling borrower who pays in full and on time. And more often than not, the zombie company has a charismatic CEO or founder who can charm lenders.

Now, there are perfectly understandable, human reasons for this. No one wants to force people out of their homes or put a company out of business and leave its workers jobless. But capitalism requires both creation and destruction. Keeping zombies alive hurts healthy companies. BIS found it actually reduces productivity for the entire economy.

The other side is that lenders must lose their money, too. Those who make irresponsible lending decisions have to face market discipline or they will keep doing it, causing further problems. Unfortunately, we do the opposite. Bailouts and monetary stimulus over the last decade generated a lot of unwise lending that is not going to end well.

Many (possibly most) of these zombie companies should fail. Or, more accurately, they will fail either suddenly in a crisis, or in slow motion if their lenders won’t bite the bullet. There really are no other options. And when they do, it will hurt not only their lenders but their suppliers, workers, and shareholders.

That, my friends, is how recessions begin. If we’re lucky, it will occur gradually and give us time to adapt. But more likely, given high leverage and interconnected markets, it will spark another crisis.

Now a Bank of America Merrill Lynch study finds roughly the same thing: 13% of developed-country public companies can’t even cover their interest payments. They are either borrowing more cash to pay off previous loans, or issuing equity to hopeful (too hopeful) investors.

While it’s easy to say these investors are making poor decisions, they’re not doing it in a vacuum. They’re trying to earn positive returns in a world where central bankers have made positive returns an endangered species. This means everyone is operating with distorted information and incentives. We’re in a hall of mirrors, so no surprise some people crash into the glass.

None of this is “natural.” It’s not the free market gone wild. It is the result of a manipulated market. The manipulators are what went wild. Sadly, they’ve only just begun…

We have another problem I also described recently: Capitalism Without Competition. A large and growing part of the economy is effectively “owned” by powerful monopolies or oligopolies that face little competition. They have no incentive to deliver better products at lower prices or to get more efficient. They simply rake in cash from people who have no choice but to hand it over.

This would be impossible if we had true capitalism, at least as Adam Smith, et al., envisioned it. Even if we generously concede that some businesses really are natural monopolies, most aren’t. The industries we now see dominated by a handful of companies got that way because the incumbents found some non-capitalistic flaw to exploit.

In theory, this problem should solve itself as technology and consumer preferences change the conditions that let the monopolies arise. Yet it isn’t happening. Axios outlined the problem in a recent article on farm bankruptcies.

Across industries, the U.S. has become a country of monopolies.

- Three companies control about 80% of mobile telecoms. Three have 95% of credit cards. Four have 70% of airline flights within the U.S. Google handles 60% of search. The list goes on. (h/t The Economist)

- In agriculture, four companies control 66% of U.S. hogs slaughtered in 2015, 85% of the steer, and half the chickens, according to the Department of Agriculture. (h/t Open Markets Institute)

- Similarly, just four companies control 85% of U.S. corn seed sales, up from 60% in 2000, and 75% of soy bean seed, a jump from about half, the Agriculture Department says. Far larger than anyone — the American companies DowDuPont and Monsanto.

As we have reported, some economists say this concentration of market power is gumming up the economy and is largely to blame for decades of flat wages and weak productivity growth.

“Gumming up the economy” is a good way to describe it. Competition is an economic lubricant. The machine works more efficiently when all the parts move freely. We get more output from the same input, or the same output with less input. Take away competition and it all begins to grind together. Eventually friction brings it to a halt… sometimes a fiery one.

The normal course of events, when politicians and central banks don’t intervene, is for companies to grow their profits by delivering better products at lower prices than their competitors. It is a dynamic process with competitors constantly dropping out and new ones appearing. Joseph Schumpeter called this “creative destruction,” which sounds harsh but it’s absolutely necessary for economic growth.

With creative destruction now scarce as zombie companies refuse to die and monopolies refuse to improve, we also struggle to generate even mild economic growth. I think those facts are connected.

Uncreative Destruction

Some of this happened with good intentions. Creative destruction means companies go out of business and workers lose their jobs. Maybe a new competitor will hire them eventually, but they suffer in the meantime. Politicians try to help but finding the right balance is hard.

I assign greater blame to the central bankers, not just the Fed but its peers as well. For whatever theoretically good reason, they kept short-term stimulus measures like QE, ZIRP, and in some places NIRP in place far too long. The resulting flood of capital short-circuited the creative destruction process.

A lot of this happens under the radar. You’ve probably seen stories about the Lyft IPO and other unicorns that will soon go public. This is news because it’s now so unusual. The number of listed companies is shrinking because a) cheap capital lets them stay private longer and b) the founders and VCs often “exit” by selling to a larger, cash-flush competitor instead of going public. An economy in which it is easier and cheaper to buy your competitors rather than out-innovate them is probably headed toward stagnation.

It is almost a sidebar, but this concept of “scale” is another important point. My usually-bearish friend Doug Kass wrote this week that Amazon will be at $3,000 within a few years and $5,000 by 2025. If it was anybody but Doug Kass I would have probably ignored such massively bullish analysis.

I won’t summarize his entire letter here, but the thought it triggered in me was that Amazon now has scale. How do you compete with that?

I was in southern Wisconsin on Tuesday, meeting with a group of current and potential investors in biotech company Galectin Therapeutics (GALT). I have a little skin in that game, so I took a day between meetings. After dinner I was talking with some of my fellow attendees. I asked one what he did and he is in the business of trying to merge or buy his competitors. Because the world now demands that he become bigger and leaner, he has to create “scale” or die. It was in a business that I didn’t think was naturally demanding scale.

The host for our Wisconsin meeting was Dick Uihlein. If you are in North America, you have probably bought something from Uline. Shipping boxes, tape, janitorial supplies, you name it. They have more than a dozen huge warehouses stocked with everything you can imagine. Their motto is order it today, get it tomorrow. And they make it work. Walking into one warehouse that is literally a quarter-mile long, that is so clean you could eat off the floor, and watching small orders literally flow from the 20-foot stacked shelves and rows hundreds of feet long, is amazing. They are growing at 14% a year and are now $8 billion+. (The fact that Dick and Liz Uihlein are two of the greatest and most generous humans on the planet does my heart good…)

But literally, how do you compete with companies like Uline and others like them? Technology and great management create scale that dominates the potential market… and make it difficult for new competition.

Between technology and ultracheap money we have short-circuited Schumpeter’s creative destruction. It is like watching the small farmer disappear. Your heart is with them but the market demands scale. Can small farmers producing locally grown food survive? Absolutely. But it is a niche market, favoring entrepreneurial farmers, not the average small farmer of yesteryear. That world is gone.

And as the world demands scale, cheap money helps it go even faster. Understand this: Cheap money is not going away. Neither is technology and the drive for scale. We can cheer for the “small farmer,” but the reality is that the world is moving to fewer competitors and larger businesses. And as I write that, I literally find myself sighing. I hate writing those words. But I can’t avoid reality. The world is changing and we must deal with it.

You may have heard about “helicopter parents,” hovering over their children to ward off any and all threats. The problem is they keep the children from gaining independence. Similarly, helicopter monetary and fiscal policy that seeks to protect the economy can instead accomplish the opposite.

Access to capital is necessary for economic growth, but free and/or subsidized capital is its long-term enemy. Managers and entrepreneurs have less incentive to innovate and operate efficiently when they can always count on another VC funding round or leveraged loan. When they don’t actually have to compete with more innovative competitors thanks to low-cost capital and their huge scale, creative destruction gets short-circuited. We no longer live in the world Schumpeter envisioned.

That’s not a complaint, just reality. I am old enough to have read numerous stories lamenting the small farmer’s demise. And I sympathetically read them, agreeing it was sad, yet happily buying lower-priced food. “Scale” in so many businesses really matters.

This doesn’t mean the Fed should keep interest rates extra-high. That would create different problems. The real barrier is this group of people who sit around a table in Washington and make decisions affecting the entire economy. That’s bad enough, but they do it based on incomplete data and flawed models.

This is a terrible situation but here’s the worst part: It isn’t going to change.

The Fed will keep manipulating interest rates downward, capital will stay cheap, businesses will keep wasting it and investors will keep believing this time is different. They’ll be partly right. This time will be different but not in the happy way they think.

The result will be a US economy that increasingly resembles Japan’s… stuck in a loop, dependent on other countries over which it has little influence or control, with an economy going sideways while a demographic tidal wave strikes.

Where does that lead? For Japan, it’s meant 30+ years in a holding pattern. I’m not sure the US will be so lucky. But at the very least, we’re going to see a decade of little or no growth and a whole lot of pain.

We could have avoided this by accepting a little more pain in the last recession. In hindsight, I’m not sure QE accomplished anything useful. For capitalism to work, lenders who make poor decisions must lose their money, not get bailed out. While I reluctantly agreed that QE1 was sadly necessary (in the words of my friend Paul McCulley, it was “responsibly irresponsible”), I still believe QE2 and QE3 were overkill. Central bankers gone wild… And not just in the US…

Our incentive structures are now so distorted I don’t see any way out. A much bigger crisis is coming and it’s going to hurt. You can either deny it or prepare for it. I know which I’m doing.

NOTICE Information on these pages contains forward-looking statements that involve risks and uncertainties. Markets and instruments profiled on this page are for informational purposes only and should not in any way come across as a recommendation to buy or sell in these assets. You should do your own thorough research before making any investment decisions. MATASII.com does not in any way guarantee that this information is free from mistakes, errors, or material misstatements. It also does not guarantee that this information is of a timely nature. Investing in Open Markets involves a great deal of risk, including the loss of all or a portion of your investment, as well as emotional distress. All risks, losses and costs associated with investing, including total loss of principal, are your responsibility.