NOMURA SHOWS "THE MOMENT EVERYTHING BROKE"

A PUBLIC SOURCED ARTICLE FOR MATASII (SUBSCRIBERS-RESEARCH & PUBLIC ACCESS ) READERS REFERENCE

MATA: PATTERNS

11-28-18 - "Nomura Shows "The Moment Everything Broke""

MATASII TAKEAWAYS:

- "the moment everything broke" took place just as October rolled in,

- ALSO READ MATASII POST: "DEALERS ARE HOARDING COLLATERAL" AT A RATE NOT SEEN "SINCE THE WORST DAYS OF 2008"

- It is debatable what catalyzed it:

- POWELL'S SPEECH: Some will point to Powell's October 4 "we may go past neutral" speech (which we discussed in "Fed Chair Powell Hints He May Soon Crash The Market");

- FULL QT RATE: Others note that this is precisely when central bank liquidity took another major step lower as the Fed's maximum quantitative tightening kicked in (as the balance sheet run off increased from $40Bn to its maximum $50Bn per month), when the ECB's bond purchase tapered from €30Bn to €15Bn/month and the BOJ stealth tapered via its YCC 'tweak.'

Whatever the reason, it was then that:

- Between sliding risk assets,

- Sharply tighter financial conditions,

- US inflation expectations via 10Y Breakevens collapsed,

- The first cracks in long/short hedge fund performance appeared,

- The CTA trend index snapped,

- Beta market neutral funds broke down and

- Risk-parity stopped working as the correlation between stocks and bonds inverted.

"but now too about the negative trajectory of US economic numbers into a more “data-dependent” Fed."

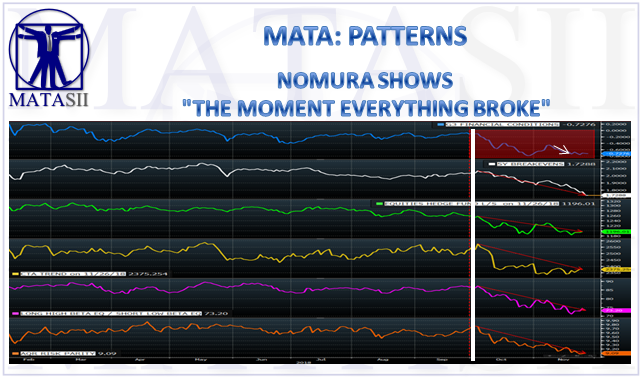

Nomura Shows "The Moment Everything Broke"

With the exception of the VIXtermination event in early February which followed a euphoric blow-off top at the end of January, the US stock market for most of 2018 was relatively smooth sailing for most traders, with the S&P - largely oblivious to events in the rest of the world - hitting an all time high on Sept. 20. And then everything changed.

As Nomura's Charlie McElligott writes, "the moment everything broke" took place just as October rolled in.

(ALSO READ MATASII POST: "DEALERS ARE HOARDING COLLATERAL" AT A RATE NOT SEEN "SINCE THE WORST DAYS OF 2008")

It is debatable what catalyzed it:

- POWELL'S SPEECH: Some will point to Powell's October 4 "we may go past neutral" speech (which we discussed in "Fed Chair Powell Hints He May Soon Crash The Market");

- FULL QT RATE: Others note that this is precisely when central bank liquidity took another major step lower as the Fed's maximum quantitative tightening kicked in (as the balance sheet run off increased from $40Bn to its maximum $50Bn per month), when the ECB's bond purchase tapered from €30Bn to €15Bn/month and the BOJ stealth tapered via its YCC 'tweak.'

Whatever the reason, it was then that:

- Between sliding risk assets,

- Sharply tighter financial conditions,

- US inflation expectations via 10Y Breakevens collapsed,

- The first cracks in long/short hedge fund performance appeared,

- The CTA trend index snapped,

- Beta market neutral funds broke down and

- Risk-parity stopped working as the correlation between stocks and bonds inverted.

This is shown in the chart below.

And once "everything broke" at the start of October, speculation that the Fed will soon be forced to stop its tightening cycle started to grow, peaking this week with traders quietly hoping that either Clarida, Powell or tomorrow's Fed minutes would hint that the Fed is relenting on its "dot plot" projections which still expect 3 rate hikes in 2019.

Meanwhile, as Nomura's Charlie McEllgiott writes, despite expectations for a “balanced, data-dependent” tone from Fed Chair Powell today (in-line with Clarida yesterday), the March 19 implied hike probability has now "shockingly" diped to now just 48% as the market buys-into the “Fed Pause” thesis.

Furthermore, overnight news flow has added further “unease” on the Fed path:

- Trump’s interview with the WaPo released last night where he stated that he was not “even a little bit happy with my selection” of Powell, adding that the Fed’s current stance on rates was “way off base”—all on top of his interview with the WSJ where he accused the Fed of being a “bigger problem than China”

- An overnight report from Bloomberg stating that Treasury Secretary Mnuchin was “said to” ask the TBAC whether they want the Federal Reserve to tighten monetary policy by raising interest rates or through faster cuts in its securities portfolio at their Oct 30th meeting—seen as a way of suggesting a way for the central bank to accomplish their goals of avoiding an “overheated economy” without triggering further ire from the President (which ironically would drive an even larger negative impact to risk-assets than further hikes in my personal view)

However, as McEllgiott argues, the "Fed Pause" thesis is not simply about weaker Equities (MXWO and SPX -8.5% from start Oct), wider Credit (US IG OAS to 22m wides), and subdued Inflation Expectations (WTI -32% since Oct 3rd and breakevens collapsing to 1Y lows) or, ironically, pressure from Trump,

"but now too about the negative trajectory of US economic numbers into a more “data-dependent” Fed."

Indeed, as shown in the chart below, the Bloomberg Economic Surprise Index has once again pivoted into outright negative territory for the first time in ~14 months after the recent misses in:

- Industrial Production,

- NAHB Housing,

- U. Michigan Sentiment,

- Cont Claims,

- Jobless Claims,

- Durable Goods and

- Dallas Fed Manufacturing,

- New Home Sales disaster

- …while internationally, we see the (consolidated) Global Manufacturing PMI Index down 9 of 10 months and at outright two year lows

Ultimately, this will force the Fed to end its normalization cycle, in turn steepening UST curves as the “risk off” signal ahead of the next recession, which will officially begin some time in mid- to late- 2019.