RESTRUCTURING LEGEND WARNS OF CORPORATE DEBT BEING THE CATALYST FOR THE NEXT FINANCIAL "PERFECT STORM"

Two months-ago, we brought to your several very concerning quotes from some of the nation's top restructuring bankers, of which the most dire warning came from Bill Derrough, the former head of restructuring at Jefferies and the current co-head of recap and restructuring at Moelis who admitted that: "I do think we're all feeling like where we were back in 2007. There was sort of a smell in the air; there were some crazy deals getting done. You just knew it was a matter of time."

What he is referring to is not just the overall level of exuberance, but the lunacy taking place in the bond market, where CLOs are being created at a record pace, where CCC-rated junk bonds can't be sold fast enough, and where the a yield-starved generation of investors who have never seen a fair and efficient market without Fed backstops, means that the coming bond-driven crash will be spectacular.

"Even if there is not a recession or credit correction, with the sheer volume of issuance there are going to be defaults that take place," said Neil Augustine, co-head of the restructuring practice at Greenhill & Co. He is right: as we showed recently using the following chart from Credit Suisse, after languishing around 1%-2% for years, default rates have jumped the most in 5 years, and are now "ticking higher."

Fast forward to today when another Wall Street legend, Jim Millstein, the banking veteran who was the restructuring chief at the U.S. Treasury Department during the 2008 financial crisis and who yesterday agreed to sell his restructuring firm to Guggenheim Partners, said the next economic downturn could now strike in less than two years, and in an interview with Bloomberg TV, warned that the US trade wars currently being waged are likely to "reduce business investment, increase costs to consumers and producers in the U.S. and reduce the sales opportunity for U.S. producers."

Previously, Guggenheim's CIO Scott Minerd said he expects a recession within two years, citing mounting corporate debt that would likely spur more defaults and a sharp decline in employment, and in a tweet earlier this week warned that "Markets are crazy to ignore the risks and consequences of a #tradewar. This rally in #stocks is the last hurrah! Investors should sell now, speculators may do better in August."

However, besides some rather vague concerns about a broader economic slowdown, Millstein also listed the specific catalyst for the next crisis: the record amount of piled up debt that has been piling up on corporate balance sheets in the past decade during periods of record low rates.

He said that the mounting wall of debt in corporate America could spur a downturn because higher interest rates constrain investments, and warned that the excessive use of leverage in the technology and industrial industries make them vulnerable if the economy worsens, calling the convergence of so many negatives a “perfect storm.”

“This is a very scary scenario,” he said. “There’s going to be real financial distress.”

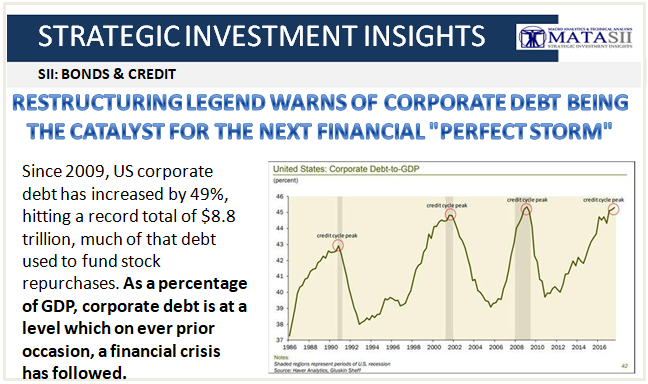

To those unfamiliar with the dynamic, here is what happened: since 2009, the amount of debt accumulated by global, non-financial junk-rated companies has soared by 58% representing $3.7 trillion in outstanding debt, the highest ever, with 40%, or $2 trillion, rated B1 or lower. Putting this in contest, since 2009, US corporate debt has increased by 49%, hitting a record total of $8.8 trillion, much of that debt used to fund stock repurchases. As a percentage of GDP, corporate debt is at a level which on ever prior occasion, a financial crisis has followed.

The coming debt deluge is also the reason why Guggenheim was eager to purchase Millstein's restructuring advisory firm: when the next recession hits, traditional banking revenue streams will collapse leaving restructuring advisories as the only winner.