THE CRITICAL TAKEAWAYS FROM THE US "YIELD SHOCK"

-- SOURCE: 10-04-18 Nomura, Bilal Hafeez - "3 Important Takeaways From The US Yield Shock" --

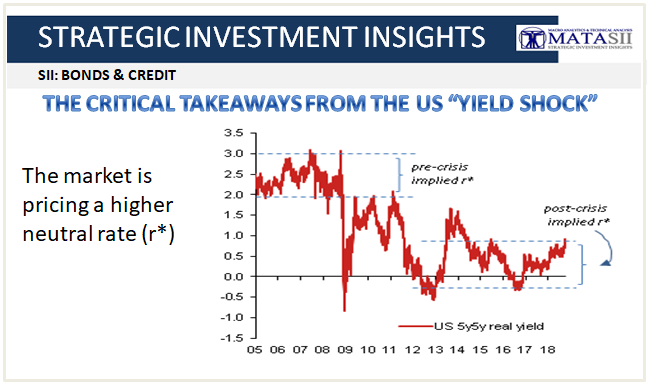

KEY MESSAGES

- The market is pricing a higher neutral rate (r*),

- Euro real yields have also moved,

- The real story could be higher Japanese 10 Year yields

Many are likely to claim credit for calling the recent surge in UST 10yr yields. Not only that, but the reason for the move will vary...

Some will say it was due to:

- Strong US data or

- Hawkish Fed or

- Return of Term Premia or

- Technical Factors such as:

- Heavy corporate issuance or

- Mortgage convexity hedging or

- The blow-out in dollar funding basis.

While there is some truth in each one of them, there are other more important takeaways from the move:

1. The market is pricing a higher neutral rate (r*).

Both the real and nominal US real curve have steepened sharply. So the 5y5y US swap real yield has jumped and appears to be breaking out of its range of recent years (see Figure 2). This suggests the market could be pricing a higher neutral rate for the Fed or even a return to the pre-crisis regime. The fact that recent Fed speakers have softened their rhetoric on their own estimates of the neutral rate could have been the context for the market to decouple from previous guidance and try to establish a level.

In macro terms, we think it means the market is starting to price the end of the secular stagnation narrative, even before we have had time to see whether the US economy will be able to cope with the end of fiscal stimulus next year. Crucially, the rates markets are driving real yields higher, meaning tighter financial conditions now too.

2. Euro real yields have also moved.

While tempting to see recent rise as a uniquely US phenomenon – short-term euro real yields have also been moving. So while UST 10yr nominal yields are breaking to new highs – the real 2yr rate differential, a measure of relative monetary policy stances, between the euro area and the US is not breaking out (see Figure 3). In fact, that spread was moving significantly against the euro up until the summer, but recently has been consolidating. This suggests higher UST yields may not be a bullish dollar story against the euro.

3. The real story could be higher Japanese 10yr yields.

Japanese yields have broken 15bp for the first time since early 2016. The BOJ’s scaling back of bond purchases, rising core inflation and concerns about the liquidity of the cash market have all been contributed to this rise. Now with global yields marching higher, Japanese rates could move further up. As a result, we are now in an environment where yields in the US, euro area and Japan are rising in unison.

This like the rise in UST real yields does not augur well for risk markets. More specifically for fall-out from higher yen rates, crosses such as AUD/JPY could increasingly come under pressure as Japan’s search for yields overseas starts to wane (see Figure 4 above).