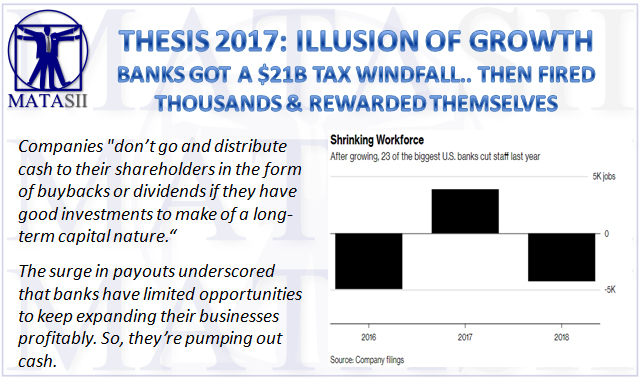

Companies "don’t go and distribute cash to their shareholders in the form of buybacks or dividends if they have good investments to make of a long-term capital nature."

On average, the banks saw their effective tax rates fall below 19 percent from the roughly 28 percent they paid in 2016.

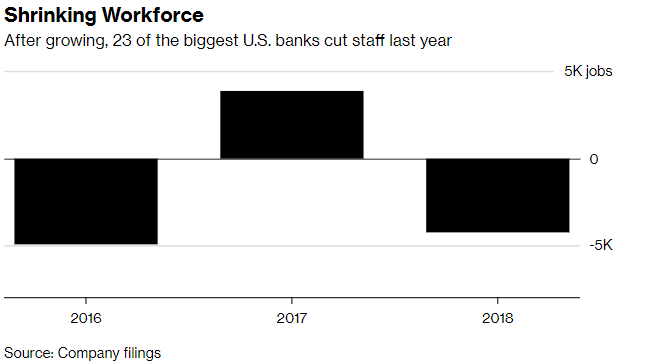

While the breaks set off a gusher of payouts to shareholders, firms cut thousands of jobs and saw their lending growth slow. -Bloomberg

The 23 firms boosted dividends and stock buybacks 23% and slashed thousands of jobs with a few signaling that more layoffs are in store.

Wells Fargo and Bank of America slashed nearly 4,900 and 4,000 jobs last year - only to be outdone by Citigroup's 5,000 job cuts.

While the banks did not provide regional breakdowns, press reports reveal that at least some of the cuts were international.

More cuts are on the horizon as well.

State Street Corp announced in January that it will be laying off 1,500 people thanks to automation,

Citigroup may cut thousands of staff from their technology and operations areas in the coming years.

As customers are being shifted to mobile platforms and new technologies to handle banking needs, the many banks have announced increased investments in automation.

"The ratio of personnel costs to revenue declined as banks gave workers a smaller slice of the money they brought in."

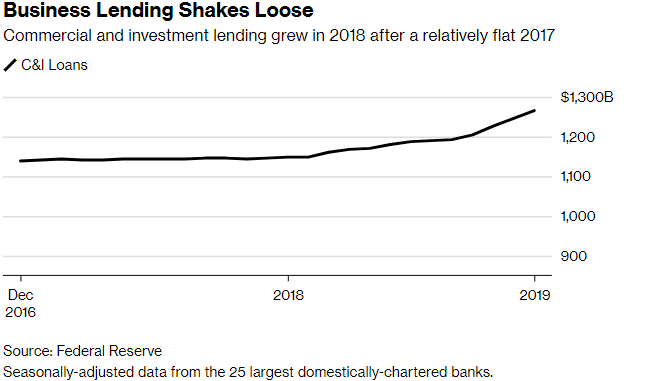

Customers also, did not benefit significantly from Banks' tax windfall - as loan portfolios only increased by 2.3% in 2018 vs. 3.6% a year earlier.

The KBW Bank Index of the nation’s largest lenders tumbled 20 percent last year.

The surge in payouts underscored that banks have limited opportunities to keep expanding their businesses profitably. So, they’re pumping out cash.

The bank index has rebounded 13 percent this year, helped by the payouts and record results.

Banks Got A $21 Billion Tax Windfall... Then Fired Thousands And Rewarded Themselves

Last year major US banks were able to cut their collective tax bill by around $21 billion thanks to the GOP tax overhaul - nearly double the budget for the entire IRS, then fired thousands of employees and tightened lending standards, reports Bloomberg.

By year-end, most of the nation’s largest lenders met or exceeded their initial predictions for tax savings. On average, the banks saw their effective tax rates fall below 19 percent from the roughly 28 percent they paid in 2016. And while the breaks set off a gusher of payouts to shareholders, firms cut thousands of jobs and saw their lending growth slow. -Bloomberg

Bloomberg's analysis is based on the financial results and commentary from 23 of the most important US banks to the nation's economy, according to the Federal Reserve. The tax windfall was not unexpected, as banks had been paying higher than average effective tax rates vs. non-financial companies.

The financial industry promised to pass the savings along to employees, small businesses and communities in need of financial help. Instead, the 23 firms boosted dividends and stock buybacks 23% and slashed thousands of jobs with a few signaling that more layoffs are in store.

Bloomberg breaks down exactly how bank employees and customers fared following the tax windfall.

Employees were a mixed bag. Of bank employees who kept their jobs, some got bonuses - such as 145,000 Bank of America workers who received $1,000 bonuses last year. Wells Fargo rewarded their poorest employees by boosting minimum wage to $15 an hour.

That said, Wells Fargo and Bank of America slashed nearly 4,900 and 4,000 jobs last year - only to be outdone by Citigroup's 5,000 job cuts. While the banks did not provide regional breakdowns, press reports reveal that at least some of the cuts were international.

More cuts are on the horizon as well. State Street Corp announced in January that it will be laying off 1,500 people thanks to automation, while Citigroup may cut thousands of staff from their technology and operations areas in the coming years.

As customers are being shifted to mobile platforms and new technologies to handle banking needs, the many banks have announced increased investments in automation.

Those employees who weren't fired received an average raise of 3.6% last year among the 23 banks surveyed. Bank of America, for example, boosted its bonuses last year to encompass more employees. That said, "the ratio of personnel costs to revenue declined as banks gave workers a smaller slice of the money they brought in."

Customers, meanwhile, did not benefit significantly from Banks' tax windfall - as loan portfolios only increased by 2.3% in 2018 vs. 3.6% a year earlier.

To be sure, lending is driven by demand from qualifying customers. Rising interest rates discouraged home sales and potentially other activities. Corporate clients also got a tax break, leaving them more money to fund expansion without borrowing.

Commercial and industrial lending -- which helps fuel job creation -- was stagnant heading into the year before picking up in the final months. That’s a sign that tax reform helped sustain economic growth, said Peter Winter, who covers regional banks for Wedbush Securities Inc. “The credit quality is still very strong for the banks,” he said. -Bloomberg

As we reported on Monday, the latest Senior Loan Officer Opinion Survey (SLOOS) by the Federal Reserve, which was conducted for bank lending activity during the fourth quarter of last year, and which reported a double whammy of tightening lending standards and terms for commercial and industrial loans on one hand, and weaker demand for those loans on the other. Even more concerning is that banks also reported weaker demand for both commercial and residential real estate loans, echoing the softer housing data in recent months.

Via Goldman:

20% of banks surveyed reportedly widened spreads of loan rates over the cost of funds for large- and medium-sized firms, while 16% narrowed spreads. 14% of banks surveyed reported higher premiums charged on riskier loans, while 4% reported lower premiums. Other terms, such as loan covenants and collateralization requirements, remained largely unchanged. Demand for loans reportedly weakened on balance.

Relative to the last survey, standards on commercial real estate (CRE) loans tightened on net over the fourth quarter of the year. On net, 17% of banks reported tightening credit standards on loans secured by multifamily residential properties, while 13% of banks on net reported tightening standards for construction and land development loans. As above, banks reported that demand for CRE loans across a broad range of categories moderately weakened on net.

Banks reported that lending standards for residential mortgage loans remained largely unchanged on net in 2018Q4 relative to the prior quarter. However, this benign environment was largely as a result of slumping demand for credit, as banks reported weaker demand across all surveyed residential loan categories, including home equity lines of credit.

While banks reported that lending standards on consumer installment loans and autos remained largely unchanged, banks reported that lending standards for credit cards had tightened slightly. Here too demand - for all categories of consumer loans - was moderately weaker, while respondent willingness to make consumer installment loans tumbled to the lowest value since the financial crisis.

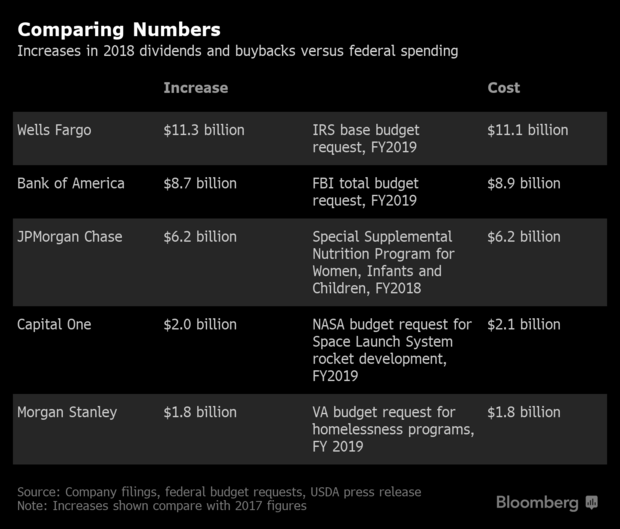

The biggest winners were shareholders, according to Bloomberg's analysis - as the six largest banks surpassed $120 billion in combined profits last year, while dividends and stock buybacks surged by an additional $28 billion over 2017 - an amount greater than their tax savings.

Many banks won Fed permission in June stress tests to boost future payouts, which means investors haven’t yet received the full benefit. (Most companies disclosed how much they paid out last year, and for those that didn’t, Bloomberg calculated it based on their shares outstanding, their stated dividends, and for two banks, their commentary on buybacks.)

Still, the KBW Bank Index of the nation’s largest lenders tumbled 20 percent last year. The surge in payouts underscored that banks have limited opportunities to keep expanding their businesses profitably. So, they’re pumping out cash. The bank index has rebounded 13 percent this year, helped by the payouts and record results. -Bloomberg

According to Dan Alpert - a Westwood Capital managing partner and senior fellow in financial macroeconomics at Cornell Law School, companies "don’t go and distribute cash to their shareholders in the form of buybacks or dividends if they have good investments to make of a long-term capital nature."

After Senators Chuck Schumer and Bernie Sanders blasted the corporate stock buybacks in a NYT Op-Ed this week, Goldman CEO Lloyd Blankfein defended how banks used cash, tweeting on Tuesday: "A company used to be encouraged to return money to shareholders when it couldn't reinvest in itself for a good return. The money doesn't vanish, it gets reinvested in higher growth businesses that boost the economy and jobs. Is that bad?"

Lloyd Blankfein

✔@lloydblankfein

A company used to be encouraged to return money to shareholders when it couldn't reinvest in itself for a good return. The money doesn't vanish, it gets reinvested in higher growth businesses that boost the economy and jobs. Is that bad?

NYT Opinion

.@SenSchumer & @SenSanders argue that when corporations dedicate so much of their resources to buying back shares, they restrain their capacity to reinvest profits more meaningfully https://nyti.ms/2Dct6pq

Bloomberg's analysis is based on the financial results and commentary from 23 of the most important US banks to the nation's economy, according to the Federal Reserve. The tax windfall was not unexpected, as banks had been paying higher than average effective tax rates vs. non-financial companies.