TRUMP'S "BIG DEFICIT" ECONOMY WOULD FAIL WITHOUT FINANCIAL REPRESSION CONTINUING!

-- SOURCE: TheInstitutionalRiskAnalyst.com, Chris Whalen - "Will Jay Powell Blink On Reducing The Fed Portfolio?" --

Last week Federal Reserve Board Chairman Jerome Powell confirmed that the Federal Open Market Committee intends to keep raising short-term interest rates based upon the strength of the US economy. Powell gave no indication that he is concerned about the rapidly approaching inversion of the Treasury yield curve or what this portends for banks and leveraged investors of all stripes, including the housing finance sector.

Also last week, the Federal Deposit Insurance Corporation released the Q2 ’18 data for the US banking industry, allowing us to update readers of The Institutional Risk Analyst on the increasingly dire situation in the credit markets. Spreads are as tight as they’ve been in decades and behavior by issuers grows more absurd by the day.

Bank interest income rose 15.7% year-over-year but interest costs rose 61% between Q2’17 and Q2’18. We’ll be updating our projections for the impending peak and decline in bank net interest margins after Labor Day in The IRA Bank Book.

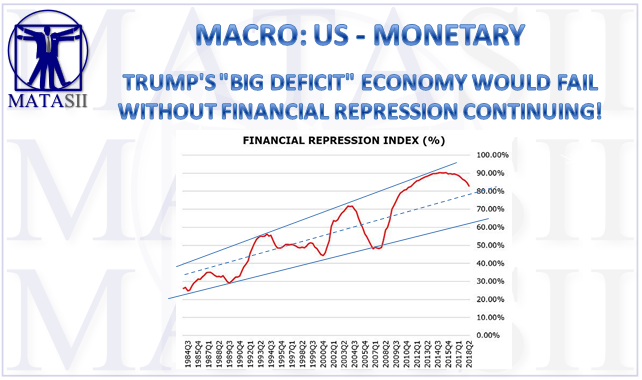

Even though the costs of funds for US banks is rising four times faster than bank interest earnings, the degree of financial subsidy -- aka "financial repression" -- to the US banking system c/o the FOMC remains massive. As the chart below illustrates, 83% of bank net interest earnings is still going to bank equity investors vs just 17% to depositors and bond holders.

Or to quote Barry Ritholtz over the weekend: “I always translate the phrase ‘financial repression’ as ‘God damn, I just missed a hell of an equities rally.’”

Banks have benefited enormously from “quantitative easing” (QE). “Net interest income totaled $134.1 billion, an increase of $10.7 billion (8.7 percent) from 12 months earlier and the largest annual dollar increase ever reported by the industry,” notes the FDIC. But strangely our favorite prudential regulator fails to note that bank funding costs rose $5 billion in Q2’18 and, by year end, interest expenses will be rising as much or even faster than are bank asset returns.

The same curve flattening dynamic that is threatening bank profitability will also severely impact REITs and other leveraged investors, which may be forced to liquidate leveraged positions. Unless and until the Fed liquidates its own portfolio down to pre-crisis levels (~ $3.2 trillion), the return on bank assets is unlikely to rise very quickly. Under the baseline scenario released by the Federal Reserve Bank of New York in April 2017, the FOMC would push bank reserves down from $2 trillion today to ~ $500 billion in 2021 in a "normalized" Fed balance sheet.

Of note, there is currently a debate inside the Fed as to whether the FOMC should slow its portfolio reduction plans in order to maintain a higher level of excess reserves. In an excellent August 14 research report entitled "The Fed's USD1.0tr question," Kevin Logan of HSBC writes:

“[R]ecent money market developments suggest that the demand for bank reserves in a normalized Fed balance sheet could be USD1trn or more, at least twice as large as the USD500bn in the New York Fed’s baseline scenario. New bank regulations imposed after the 2008/2009 financial crisis have increased the amount of high quality liquid assets (HQLA) that banks are now required to hold. Reserves held at the Fed are the ultimate in HQLA for banks. They are completely liquid and, from a credit risk standpoint, are of the highest quality.”

Logan argues that the FOMC may end its portfolio reduction program sooner than expected, perhaps by the end of 2019 because regulatory changes have made a larger excess reserve position necessary. But he also notes that:

“[S]everal academics and former Fed officials have argued that the Fed should return to a small balance sheet, one in which reserves are scarce. They argue that a large balance sheet distorts capital markets by putting unnecessary downward pressure on longer-term interest rates. A large balance sheet could also impede market functioning and the price signals coming from an active federal funds market that reflects the credit worthiness of banks involved in the market.”

Put us on the side of the academics and former Fed officials who understand that the FOMC’s expansion of excess reserves to fund its purchases of trillions of dollars in securities for QE did enormous damage to the US money markets – damage yet to be undone. Instead of encouraging banks to again buy US Treasury debt to fund liquidity requirements, the FOMC apparently prefers to further subsidize the banking industry by indefinitely providing a ready supply of risk-free assets in the form of excess reserves. But doing so also suggests that bank interest income will not rise along with the FOMC’s increase in short-term interest rates, as shown in the chart below.

We all need to remember that QE was not a form of economic "stimulus," but rather a backdoor subsidy for the US Treasury. The bonds owned by the FOMC that created the excess reserves ought to be in private hands. The Fed (and other central banks) are suppressing long-term interest rates by holding $10 trillion worth of securities, positions that are entirely passive, not financed in the private markets and also unhedged. These large portfolios of securities held by central banks are not only keeping long-term rates down, but are also responsible for tight credit spreads and low levels of secondary market activity. The only beneficiaries of QE are the growing number of governments among the G-10 nations that are headed for debt problems.

Some economists worry that providing banks with risk free reserves discourages lending, but we think the damage to the money markets is a far more grave concern. QE and “Operation Twist” have forcibly crushed credit spreads and loan profitability. Large US banks, for example, lost almost 1% net on residential production in Q2’18, according to the Mortgage Bankers Association. As in 2006, banks in the residential mortgage sector are fighting over conforming loans to put into private label securitization deals, this as lending volumes fall.

Only by gradually forcing banks to shed excess reserves and replace these risk free assets with Treasury and agency securities will the money markets again begin to operate. Of course, as excess reserves run off, the real debt load on the Treasury will grow. Do Jay Powell and the other FOMC members have the political courage to end the subsidies for the US Treasury and banks, and thereby end financial repression?

If the FOMC sticks to its guns and pushes excess reserves down to $500 billion as now planned, long term rates will rise, the functioning of private money markets will return and savers will see an increased share of the interest rate pie. Banks will trade and hedge and finance larger Treasury positions, and this private market activity will put upward pressure on long-term Treasury yields. Dealers will earn additional income from an increase in trading and hedging activity. Lenders may even start to see expansion of spreads for credit products. Then and only then, when the functioning of private markets have been restored, can the FOMC truly declare victory.