WHY THE CARPET IS ABOUT TO BE PULLED FROM UNDER THE JUNK BOND MARKET

-- SOURCE: 07-03-18 ZeroHedge - "Why The Carpet Is About To Be Pulled From Under The Junk Bond Market" --

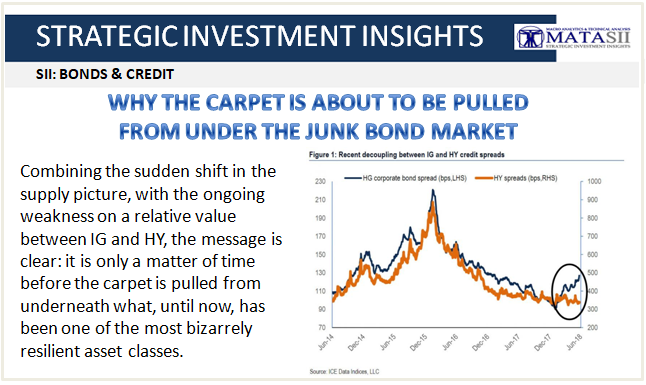

Last week we noted that ever since the start of 2018, an odd divergence has emerged in credit markets, where Investment Grade bonds have seen their spreads leak progressively wider, hitting levels not seen in 2 years, while the bid for higher yielding, and much more risky, junk bond debt has been seemingly relentless, with high yield spreads near all time lows.

There have been various reasons offered to explain this divergence, with Bank of America suggesting that IG weakness is "due to supply pressures in an environment of reduced demand that began in March and extended through last week, plus the Italian situation, which is about systemic risks running through the global IG financial system."

Meanwhile, it believes the strength in HY is mostly due to the lack of supply of higher yielding paper.

Blackrock agrees, and today, in a blog post by BlackRock's Richard Turnill, the Chief Investment Strategist picks up on this theme and writes that Investment grade (IG) bonds typically outperform their high yield counterparts when uncertainty rises - like now - given their higher quality and lower default risks.

The chart below echoes the one shown above, and confirms that recently this hasn’t been the case. The bars on the left depict the recent under-performance of IG. Yield spreads have widened versus Treasuries, putting downward pressure on prices. The move in the high yield market has been much more muted. The bars on the right show why. Actual, and anticipated, IG issuance has rapidly escalated amid a surge in mergers and acquisitions (M&A) activity, particularly in the media sector (overall IG issuance is still down just over 1% due to large repatriated cash balances providing less incentive to issue debt). Yet high yield issuance has slumped. The shrinking high yield market is not part of the M&A boom, and many high yield firms are issuing via loans rather than bonds.

Others have also jumped on the "issuance" bottleneck, with Goldman today noting that trends in the HY primary market have been closely watched this year, as a significant decline in issuance has provided a strong tailwind to spread performance.

Specifically, as the chart below shows, year-to-date HY supply of $104 billion is down 26% versus this time last year, and this favorable technical has allowed HY spreads to remain much more resilient versus IG peers. For context - and as shown in the chart on top - prior to last week, HY spreads were unchanged versus the start of the year (at 339bp) while IG spreads widened from 94bp to 123bp over the same period. HY spreads even touched multi-year lows earlier this year despite facing sizable cumulative net outflows.

The tide may be shifting, however.

According to Goldman calculations, the junk bond dam may be cracking and last week's HY new issue volumes of $7.2 billion were the highest since mid-March (Exhibit 1), and this increase in supply appeared to pressure HY market performance.

- First, the higher supply was accompanied by weakness in HY spreads. Last week saw significant decompression between IG and HY: the OAS of the Bloomberg Barclays HY index widened from 339bp to 363bp while the IG index finished unchanged on the week (Exhibit 2). While negative idiosyncratic developments for some HY issuers and escalating trade tensions likely also played a role, the spike in HY supply is one of the key drivers according to Goldman. The HY spread weakness is even more striking considering oil – an important driver of HY investor sentiment given the Energy sector's large market weight (14.4%) – rallied over 8% to close the week at $74.15 (a level not seen since 2014).

- Second, the acceleration in HY bond issuance may be related to some early signs of new issue indigestion in the leveraged loan market. According to data from LCD Research, last month, upward price-flex activity outnumbered downward price-flexes (ratio of 1.26x) for the first time since February 2016. This price-flex imbalance was even more pronounced for M&A deals (1.46x), which we believe was likely related to Q2 2018's record-setting level of institutional M&A volumes ($84.2 billion). Looking ahead, we continue to view HY M&A activity (particularly for larger deals) as the key catalyst to fuel a sustained acceleration in HY bond supply.

Looking at the recent supply burst, Goldman concludes that while it is premature to expect the large year-to-date HY supply deficit to narrow rapidly from here, especially given the seasonally slow summer months, last week's price action is indicative of the growing fragility of the HY market's (technically-supported) relative outperformance.

Today Blackrock reached a similar conclusion - get out of HY and into IG despite the recent pain - however due to more fundamental reasons: "investment grade valuations have become more attractive relative to those of high yield. Yields for short-maturity investment grade corporates are now well above the level of U.S. inflation. We see these assets again playing their traditional portfolio role—principal preservation, especially in an increasingly uncertain macro environment."

Uncertainty around the growth outlook has widened, with the U.S. stimulus’ boost to activity on one side–and trade war risks on the other. This greater uncertainty−along with rising interest rates−has contributed to tightening financial conditions and argues for higher-quality ballast in portfolios.

Combining the sudden shift in the supply picture, with the ongoing weakness on a relative value between IG and HY, the message is clear: it is only a matter of time before the carpet is pulled from underneath what, until now, has been one of the most bizarrely resilient asset classes.