IN-DEPTH: TRANSCRIPTION - LONGWave – 06-08-22 - JUNE – Peak Inflation v Gold

SLIDE DECK

TRANSCRIPTION

SLIDE 2

Thank you for joining me. I'm Gord Long.

A REMINDER BEFORE WE BEGIN: DO NO NOT TRADE FROM ANY OF THESE SLIDES - they are COMMENTARY for educational and discussions purposes ONLY.

Always consult a professional financial advisor before making any investment decisions.

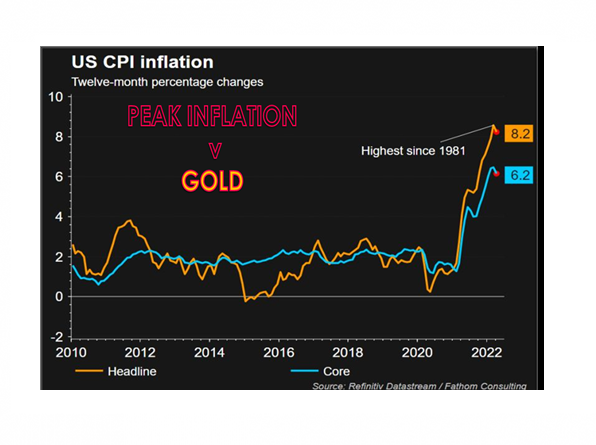

COVER

I like to focus specifically on Gold at least once a year and it has been awhile since we had the opportunity.

With the focus increasingly shifting to whether Inflation has peaked and a looming recession bringing deflationary pressures, it therefore begs the question of whether Gold has seen its better days and more downside is ahead.

With the recent weakness in Gold there appears to be real merit in this thinking.

SLIDE 4

In this session I hope to answer what is going on with gold and what we might expect going forward. I envisage three coming unique stages which we will outline.

The bottom line is you will be given an opportunity in Q3 for an excellent entry price for gold, before it leaves the station for major new highs.

As such I hope to cover the subjects listed here.

SLIDE 5

Let’s start with the current Economic trend underway (or at least the Federal Reserve narrative it is promoting) which gold is reacting to and how they relate to the trade mechanics of gold. Remember, the Fed pumped the narrative that Inflation was only “transitory” for a year, and doing nothing about it, before embarrassingly giving up on that mistaken belief.

SLIDE 6

From a big picture perspective we need to appreciate that Gold follows Yield!

As you can see in this chart from 1964 to the late 1990’s Gold followed yields as measured by the 10Y UST note.

As the 10Y UST yields in blue rose, gold followed. When UST yields reversed gold reversed and followed yields lower.

I highlighted this era because it was a particularly volatile era when the US came off the gold standard in the early 70’s, yields reached all time highs during Volcker’s Fed Chairmanship during the early 80’s and when the US rescinded the Glass-Steagall Act with the Gramm-Leach-Bliley Act of 1999. All were major events in yields and the real value of money.

SLIDE 7

I won’t take you through all the various swings in Fed yield policy over the decades but the relationship is consistent. My colleague Richard Duncan does a masterful job of laying all this out in his latest missive “Gold: If Not Now, When?”.

If you are not yet a subscriber I encourage you to do so using the special MATASII discount code “Flows”.

The net of Richards work is that the Fed’s shift to Quantitative Tightening (QT); a rising Fed Funds Rate; and an overall fight against inflation is another major inflection in Yields, on the scale of 1975, 1981 and 2016. All were bad for gold prices as this one will also be.

SLIDE 8

The resulting price drop in gold may be quite significant, if the Fed in fact follows through on it stated monetary direction and plans.

We will come back to the Fed’s plans a little later!

SLIDE 9

Let’s look at a more current correlation of Yields versus Gold. This chart covers the current 7 month period.

We see on the left that the correlation held as usual until the Ukraine conflict (shown by the grey box). At that point gold and yield separated fairly significantly. Gold surged on Geo-Political risk while yields temporarily dropped. This ended in late April with a major drop in gold which resulted in the correlation resuming –at least temporarily.

On April 18th a separation occurred again. This one was even more pronounced! Though Yields were more or less within a trading range, gold fell hard and barely able to stay above 1800.

The obvious question is WHY? Then we need to answer WHAT is therefore likely to occur next?

SLIDE 10

To answer that question we must revisit some relational market mechanics.

As we discussed, the 10Y UST Yield on a big picture is driven by Fed Monetary Policy as shown on the left.

However, there are two components in what underpins the 10Y UST nominal value. We have discussed this many times in previous videos and newsletters.

They are:

- Inflation Breakevens, and

- Real Rates

As long time subscribers are well aware the addition of the two equaling the 10Y UST Yield is the Fisher’s Equation which we have shown to work very precisely.

What is important to understand is that gold acts differently with each of these components.

- When Inflation Break-evens go up – Gold goes up

- When Real Rates go up – Gold goes down!

This is at the core of what is causing the current divergence.

SLIDE 11

Inflation Break-evens and Real Rates can be quite volatile as they are driven by sentiment. Treasury yields have been historically less volatile. However, the Fisher Equation says these two volatile drivers of gold prices must equal the less volatile movements of yields. This will cause temporary distortions and divergences.

SLIDE 12

Bear with me as we get into some detail so you can fully appreciate what is going on with gold and what therefore is likely to soon occur.

Shown here is one of the two drivers of the pricing of gold - the 10Y Break-even Inflation Rate.

Shown by the red box you can see that on Friday June 3rd the break-even inflation rate closed at 2.74%.

The red arrow highlights that starting on April 18th the Break-even rate fell quite dramatically from approximately 3.0% to 2.55% or a 45 bp drop.

When Inflation Breakevens fall – gold goes down!

SLIDE 13

That is precisely what happened.

Gold started falling significantly on April 18th. The divergence and drop in gold continued until approximately May 13th.

Let’s now look at what happened to the other driver of gold – the 10Y UST Real Rate.

SLIDE 14

You can see here that during the same period from April 18th to May 13th that the 10Y UST Real Rate rose from approximately zero to 0.25%, a 25 bp rise.

As we know, when real rates rise then gold falls!

SLIDE 15

That is exactly what happened as both drivers of gold were forcing it down.

However they were offset for the UST Yield (which is the addition of the two) forcing it into a more or less widened trading range.

You can see that as can be expected on Friday June 3rd the additions of the UST Break-even of 2.74% and the Real Rate of 18.8% gives us the UST nominal yield value of 2.93% for that date

SLIDE 16

If we explode the May trading range of the 10Y UST Yield we see this technical chart. The range on this scale says the trend was down.

Though we can’t be sure until we see this coming weeks CPI and PPI prints, we have the ear marks according to Elliott Wave Analysis of a potential Complex Combo Correction or “Zigzag” with a target of 2.5% labeled at the bottom before correcting upwards.

Obviously we can’t be assured this will happen but have added proof since this pattern is now appearing across multiple markets as a fractal signature – something we continuously look for!.

SLIDE 17

What might all this mean?

It suggests in the short term or Phase 1 we are likely to see 2.5% in the 10Y UST as the CPI and June FOMC meeting might highlight that the Fed needs to be slightly less hawkish.

We found hidden in the last FOMC minutes (and not adequately covered by the business media) was the fact that the Fed is leaning towards taking rates quickly to the neutral rate, but not necessarily any further. I suspect this will become clearer with this month’s FOMC meeting on June 14-15th.

I suspect it was also discussed when Powell was recently called to the White House. The Biden administration obviously very concerned about the upcoming mid-term fall elections and needs some economic relief going into them.

There is a strong chance that gold surges near term to $1940

SLIDE 18

You can see here that if yield headed towards 2.5% and gold rose to $1940/oz the gap would be closed. We can be assured this will not work as we postulate but we may at least be in the approximate ball-mark if the historical correlation more closely converges in the short term.

SLIDE 19

However that is the short term over the next few weeks.

What we are looking at the intermediate term is whether

- The Fed will continue with QT and

- Whether we are likely to see falling Y-o-Y Inflation comparisons appear as if Inflation has peaked.

These drivers if they occur will push gold down through at least Q3 2022.

The technical gold chart shown here suggests that this occurs until late Q3 then reverses with gold at lower levels. This would prove to be an excellent entry point.

SLIDE 20

This is because it is our view and analysis that the Fed will be forced to reverse its current monetary policy direction narrative by then to avoid a serious looming recession. We feel this in fact is the current Fed plan and are only “talking the market” euphoria down! Therefore:

- Gold will again align itself with Fed Monetary Policy as QT is halted,

- Gold will rise as the fight against Inflation is effectively sidelined to fight collapsing growth with liquidity expanding and financial conditions loosening.

SLIDE 21

This sequence would complete our long held view of the completion of a major Cup and Handle formation pattern in Gold.

We have found it interesting to see a sub-Cup and Handle fractal appear during this process.

SLIDE 22

However, there is a lot more going on in Gold than just fed Monitor Policy, Yields, Breakevens and technical patterns.

We have significant developments on other areas which influence gold.

One of those is the mechanics of a changing Supply and Demand curve!

SLIDE 23

Central Banks are now buying Gold in a major way – this is a big shift and is being accelerated by the further US weaponizing of the US dollar with its sanctions against Russia.

Countries are moving more of their FX reserves into a neutral holding of Gold not to be caught between a coming potential Cold War II between the west and a China/ Russia aligned commodity based consortium of countries.

SLIDE 24

We are seeing more global growth in Gold holding within ETF’s and from active money managers trying to diversify portfolios.

SLIDE 25

We are seeing growth in Gold ETF’s themselves as a percentage of overall US & global holdings.

Demand is growing rapidly

SLIDE 26

Meanwhile Supply has not kept up and it is highly likely to get worse due to an overall lack of investment.

The costs to bring new production online have skyrocketed and continue to discourage capita investment:

- Exploration cost are through the roof,

- Licensing, Zoning and Regulatory costs are Hugh and increasingly problematic and restrictive,

- Physical construction of bringing a new site online are going up exponentially,

- Production costs associated with labor, material, taxes etc have recently become problematic,

- Distribution costs are stripping razor thin margins,

- The time to get a new mine operational can easily take a decade.

All of this has lead to poor investment to match growing demand. Miners are more or less waiting for the inevitable to occur.

SLIDE 27

Presently all-in sustaining costs in the 1700-1900 range are fairly close to what gold is actually trading at.

SLIDE 28

But the production costs of the majors producers, as we mentioned are exploding.

We should expect gold to simple rise -- like all commodities from Energy to Food to Housing are!

40% prices increases are not at all unlikely based on what we are seeing with other commodities!

… and this assume longer term, sustained Supply shortages don’t squeeze gold even much higher!

SLIDE 29

There are also other emerging drivers of gold.

SLIDE 30

Commodities, as an asset class, are in the early stages of its own Super-Cycle.

We have chronicled this over the last couple of years and it is now becoming obvious to the investment community.

Gold, like Silver, performs both as Money and a Commodity

SLIDE 31

Gold is still a misunderstood investment. Any real changing attention given to it, because of its relatively small participation in modern portfolio management, will be profound.

-

- Gold used to be a Geo-Political Hedge. This only recently showed itself again with the Ukraine conflict. We can be assured of increasing and more dangerous Geo-Political conflicts going forward.

- More professional investment managers are increasingly adding Gold to Portfolio Diversification & Balancing strategies.

- Fiat Currencies are now under attack as China and Russia move towards increasingly supporting their currencies with hard asset backing.

- Stagflation and slow growth can be expected to foster increased allocations towards Value versus Growth.

- Never forget that Gold is money in troubling and uncertain times. Uncertainty and shortages foster the growth in Dark Money and Black Markets. Expect them which will itself pressure gold prices!

SLIDE 32

What can we conclude?

SLIDE 33

Gold is both a Commodity and Money!

A whole generation (or two) will soon re-discover this during this unfolding decade.

Fiat Currency is a relatively new phenomenon that has endured during the historically unusual stable times since the end of WWII.

Fiat Currencies have never proven themselves as viable over the long run.

Fiat Currencies are prone to collapse because they are founded on the belief and faith in governments. When that faith is shaken people historically look for something they can trust! This doesn’t mean Fiat Currencies are going away – just people confidence in them is! Investors can be expected to seek protection from this shift. Precious metals are the proven strategy for this justified fear.

SLIDE 34

No one knows with certainty where gold is headed but I don’t think the well researched and highly knowledgeable professionals at Incrementum shown here are too far off.

$5000/Oz by the end of the decade is certainly a possibility! Selling at lower than current production costs is not a possibility!

Just ask yourself - what has this sort of certainty of upside with so little downside?

SLIDE 35

As I always remind you in these videos, remember politicians and Central Banks will print the money to solve any and all problems, until such time as no one will take the money or it is of no value.

That day is still in the future so take advantage of the opportunities as they currently exist.

Investing is always easier when you know with relative certainty how the powers to be will react. Your chances of success go up dramatically.

The powers to be are now effectively trapped by policies of fiat currencies, unsound money, political polarization and global policy paralysis.

SLIDE 36

I would like take a moment as a reminder

DO NO NOT TRADE FROM ANY OF THESE SLIDES - they are for educational and discussions purposes ONLY.

As negative as these comments often are, there has seldom been a better time for investing. However, it requires careful analysis and not following what have traditionally been the true and tried approaches.

Do your reading and make sure you have a knowledgeable and well informed financial advisor.

So until we talk again, may 2022 turn out to be an outstanding investment year for you and your family.

Thank you for listening