Global Central Bank Buying Puts A Floor Under The Price of Gold

The only reason the price of gold’s down on the year is because of a strong dollar.

Actually – for how much the dollar’s rallied this year, gold holding around the $1,200 range is very bullish.

And if gold’s been able to hold its own during a stronger dollar and aggressive Federal Reserve tightening – imagine what it will do once they decide to begin easing. . .

Putting it simply – the price will soar. . .

So, who’s taking advantage of this weaker gold price?

The Global Central banks – but specifically the Emerging Markets.

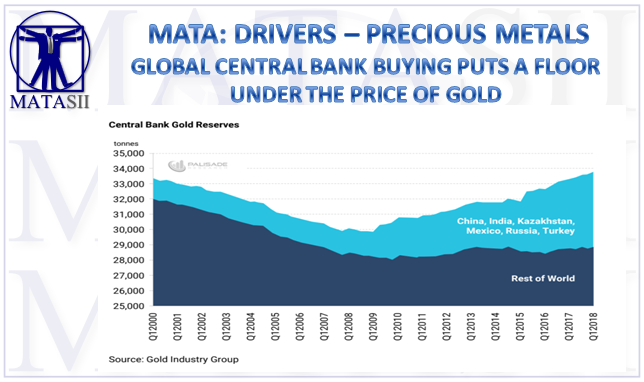

Here is the latest data showing the Q2/2018 Central Bank gold reserves.

This comes after Central Banks added 116.5 tons to their ‘official’ reserves in Q1/2018. This was the highest first quarter increase over the last four years.

It’s widely known that in the 1990’s and first decade of the new millennium – Central Bank’s were dumping their gold.

Starting in the late 1980’s, gold reserves in Central Bank vaults declined from roughly 36,000 to just under 30,000. That’s a huge drop.

To be clear, they didn’t just sell the gold. The Central Banks also engaged in the ‘gold carry trade’.

This is when Central Banks ‘lease’ their gold reserves to investment banks for a set amount of time and a bit of interest.

The investment banks then sell that gold in to the market – get dollars in return – and buy bonds or equities.

After a while, they take the profits and buy the gold back – returning it to the Central Banks.

You can see how lucrative this trade is. And how it incentivizes the investment banks to keep the gold price down (since they have to buy back the gold later to return it to the Central Banks).

Years of this extra gold supply hitting the markets caused the price of gold per ounce to drop below $250.

This lasted until 14 Central Banks got together in 1999 and agreed to limit the amount of gold sold/lent out. This is known as The Washington Agreement.

And although Central Banks continued to sell gold through the early 2000’s (you can see this in the chart above) – the price of gold still rallied from $250 in to the high $1,900’s in 2011.

Now – just imagine how high gold would have gone if Central Banks were net-buyers of gold instead of net-sellers during that time period. . .

Well, that’s exactly what’s happening today.

Global Central Bank reserves are at a 20 year high – 34,000 tones – and has been primarily driven by China, Russia, and other Emerging Markets.

After the crisis of 2008, the Emerging Markets – especially China and Russia – have been weary of the U.S. dollar’s dominance. They won’t be held hostage for what the Federal Reserve does to the U.S. dollar’s value going forward.

This is extremely important since heavy and consistent Central Bank buying is putting a floor under the price of gold.

All it takes now is just a little investment and retail demand to push the gold price much higher.

And I believe the catalyst will be when hedge funds and money managers eventually buyback the record gold and GLD shorts currently outstanding (you can read more about that here).

Gold has long-term support for higher prices. . .

That’s because Central Banks are now net-buyers (specifically the Emerging Markets). And ‘peak gold’ production is over – mine output continues declining as major gold deposits dry up worldwide.

Due to these two facts; the fundamentals for gold looks exceptionally strong from the increased demand and declining supplies.

So far, Central Banks show no signs of slowing down their buying – let alone selling it. They learned from that awful mistake last time.

Don’t expect that to happen again.