Debt with the highest AAA ratings has almost ceased to exist.

The greatest increase in debt volume by far has come in the lowest-quality investment-grade credits and in below-investment-grade.

It looks like corporate borrowers are gaming the ratings firms (and not for the first time) by making sure they borrow as much as they can while not suffering the downgrade that would lead to higher borrowing costs.

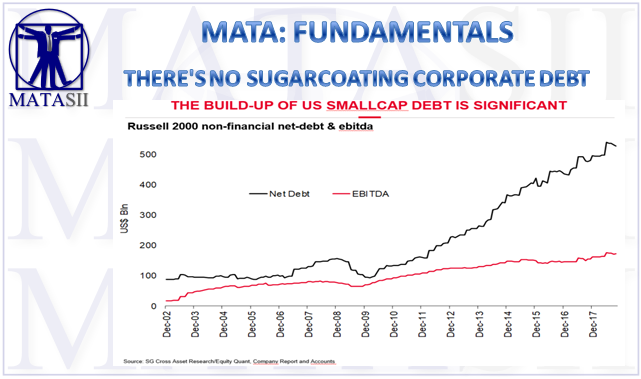

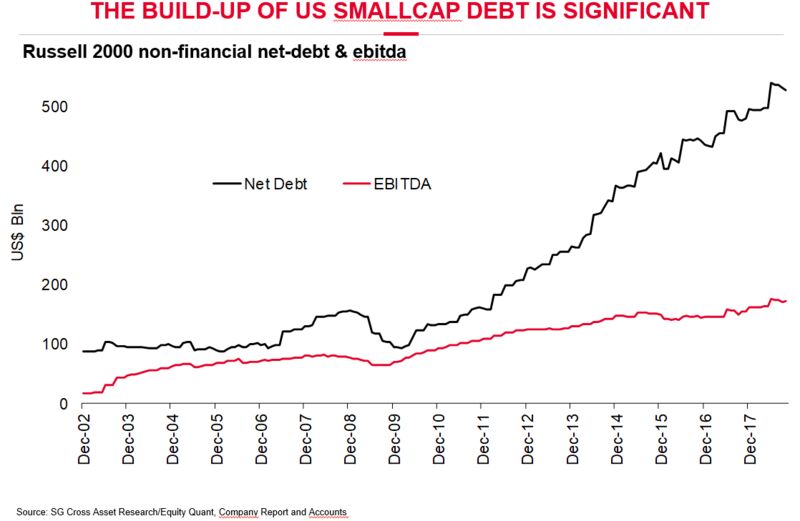

The net debt of the smaller companies in the Russell 2000 has run far ahead of their cash flows,

Non-financial corporates look almost as leveraged on this measure as they have at any time since the peak hit during the dot-com boom two decades ago.

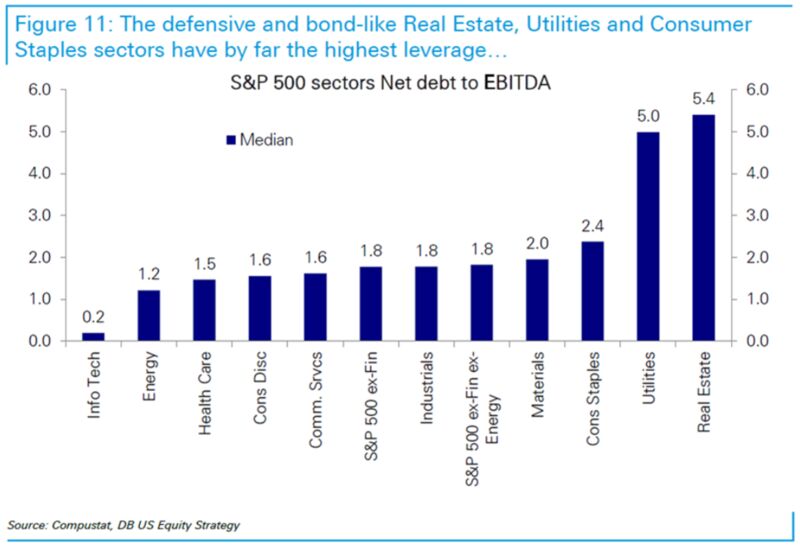

Leverage is heavily concentrated in the most relatively safe and boring sectors, led by utilities and real estate, which have reliable cash flows

However, it still appears we should be concerned about the debt that companies have taken on while interest rates have been historically low.

It looks like borrowers are gaming the ratings firms, and not for the first time.

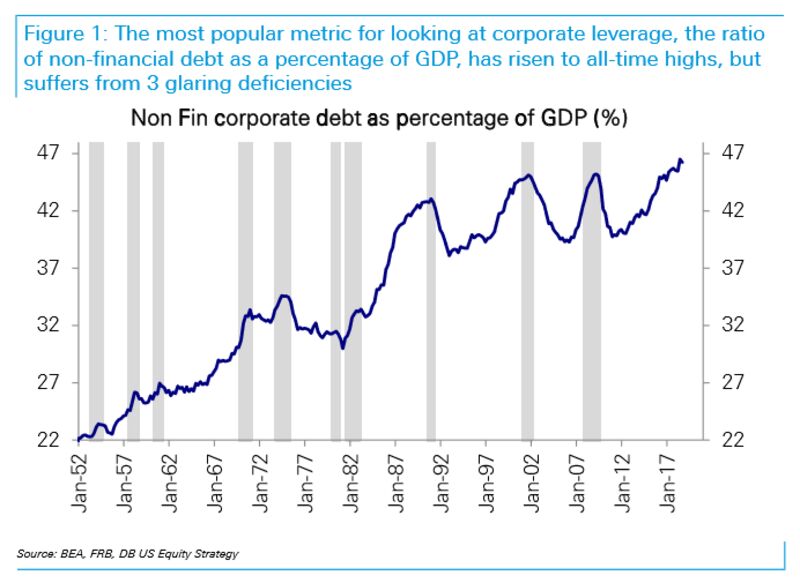

If you are looking for reasons to worry about the stock market, few things beat U.S. corporate leverage. Excluding banks, which have very different dynamics, corporate debt has never been greater as a percentage of gross domestic product.

The following chart comes from Deutsche Bank AG chief global strategist Bankim Chadha, who last week attempted in a report to show that the corporate debt issue had been overstated. He makes some very valid points, but it still appears we should be concerned about the debt that companies have taken on while interest rates have been historically low.

Chadha argues that we should be more interested in net debt, which subtracts out cash holdings, and compares that to profits rather than GDP. After all, it is from profits that the debt must ultimately be repaid. This leads to a radically different picture:

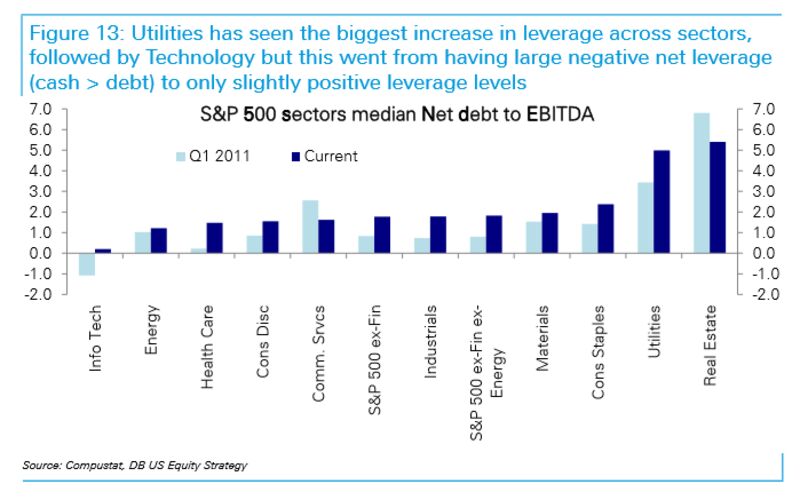

He also points out that leverage is heavily concentrated in the most relatively safe and boring sectors, led by utilities and real estate, which have reliable cash flows:

This, along with a lot of other very impressive number-crunching, stands up Chadha’s headline: “Is Corporate Leverage High? No, It’s A Sector Story.”In particular, it is a story about utilities.

On this basis, it seems there’s far less to worry about. Among the larger companies in the S&P 500, the debt has largely been taken on by those companies best placed to pay it back. The problem of over-leverage is not as sweeping or systemic as it appears.

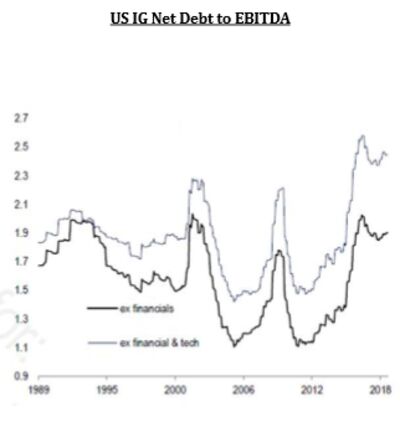

But there are still reasons for concern. Deltec produced the following analysis last month. Rather than compare to profits, which many believe to be unrealistically high, the following chart compares investment-grade net debt to earnings before interest, tax, depreciation and amortization, which is a decent measure for cash flow. Non-financial corporates look almost as leveraged on this measure as they have at any time since the peak hit during the dot-com boom two decades ago. Excluding the tech sector, where companies are able to borrow against impressively high cash flows, corporate investment-grade debt looks as though it is at a historic high. Even if the debt is primarily taken on by companies with relatively strong cash flows, it is worth asking why they did not borrow so much before:

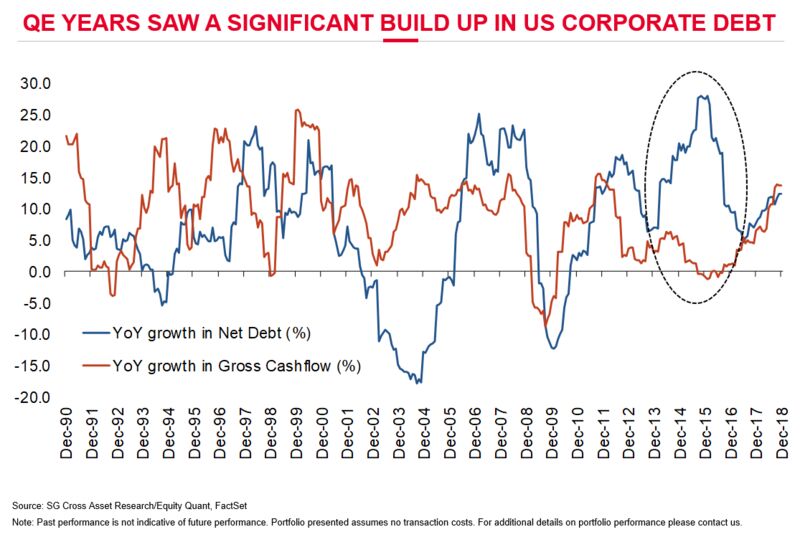

To illustrate this problem in a slightly different way, try this chart from Andrew Lapthorne, the chief quantitative strategist at Societe Generale. In the era of quantitative easing following the financial crisis, net debt has increased far faster than cash flows:

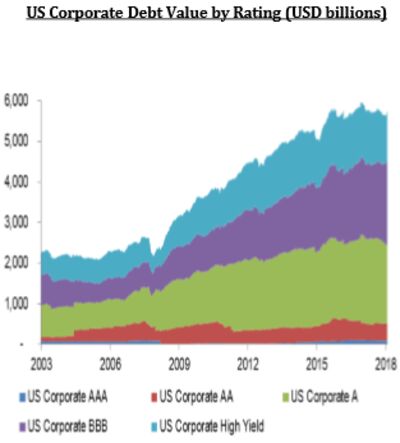

True, the problem was ameliorated a little by last year’s big repatriation of cash, but it is still an issue. A further issue highlighted by Deltec and others is the obvious and persistent dilution of credit quality. Just look at this:

Debt with the highest AAA ratings has almost ceased to exist. And the greatest increase in debt volume by far has come in the lowest-quality investment-grade credits and in below-investment-grade. It looks like corporate borrowers are gaming the ratings firms (and not for the first time) by making sure they borrow as much as they can while not suffering the downgrade that would lead to higher borrowing costs. While Chadha’s numbers are for the larger companies in the S&P 500, Lapthorne produces this alarming data showing that the net debt of the smaller companies in the Russell 2000 has run far ahead of their cash flows:

This is alarming, even if it does not imply a risk of imminent disaster for the S&P 500. The presence of leverage increases risks and it is plain that a lot of companies have taken the opportunity to stretch themselves to an unprecedented extent. Even if this corporate leverage doesn’t drive investors out of equities broadly, balance-sheet quality is likely to be a critical issue for anyone picking stocks. Avoiding the many companies that have over-levered looks imperative.

FAIR USE NOTICEThis site contains copyrighted material the use of which has not always been specifically authorized by the copyright owner. We are making such material available in our efforts to advance understanding of environmental, political, human rights, economic, democracy, scientific, and social justice issues, etc. We believe this constitutes a 'fair use' of any such copyrighted material as provided for in section 107 of the US Copyright Law. In accordance with Title 17 U.S.C. Section 107, the material on this site is distributed without profit to those who have expressed a prior interest in receiving the included information for research and educational purposes. If you wish to use copyrighted material from this site for purposes of your own that go beyond 'fair use', you must obtain permission from the copyright owner.

NOTICE Information on these pages contains forward-looking statements that involve risks and uncertainties. Markets and instruments profiled on this page are for informational purposes only and should not in any way come across as a recommendation to buy or sell in these assets. You should do your own thorough research before making any investment decisions. MATASII.com does not in any way guarantee that this information is free from mistakes, errors, or material misstatements. It also does not guarantee that this information is of a timely nature. Investing in Open Markets involves a great deal of risk, including the loss of all or a portion of your investment, as well as emotional distress. All risks, losses and costs associated with investing, including total loss of principal, are your responsibility.