The salient point from the Q1 Earnings season is that the results have not been bad enough to stop the U.S. stock market from getting back to an all-time high.

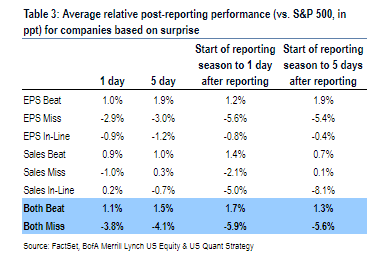

Companies that disappointed were strongly punished (with Google parent company Alphabet the latest and most spectacular example), while those that won the game of massaging expectations gained little reward.

Companies that missed on both their earnings and sales were punished with a 5.9 percent decline in their shares on average; those that managed a positive surprise on both measures gained only 1.7 percent,

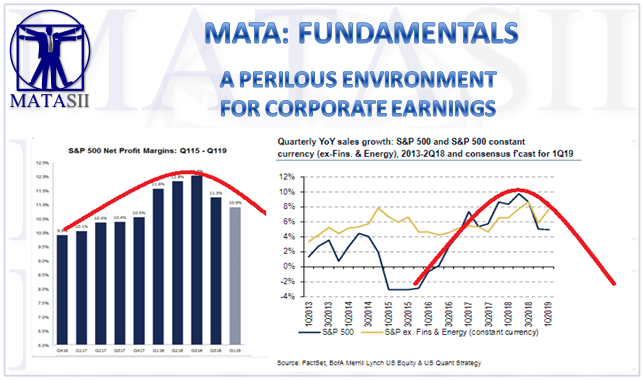

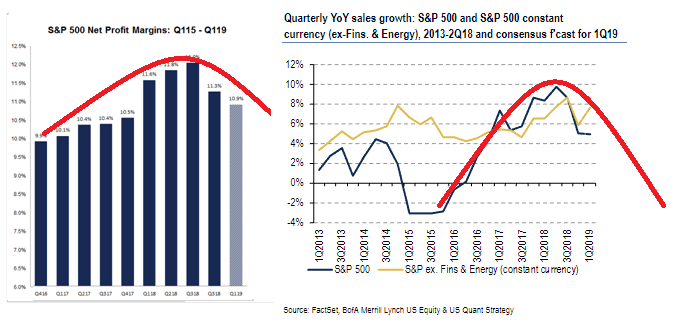

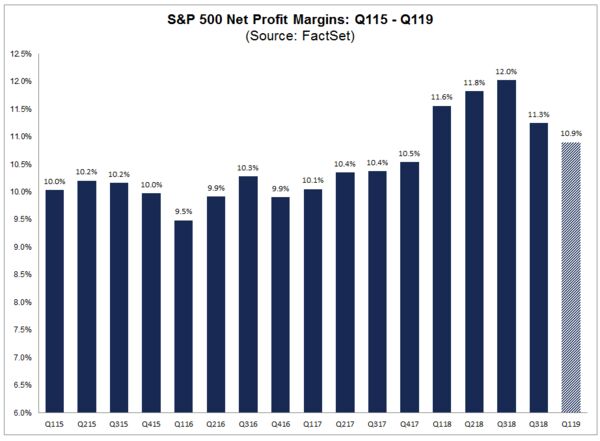

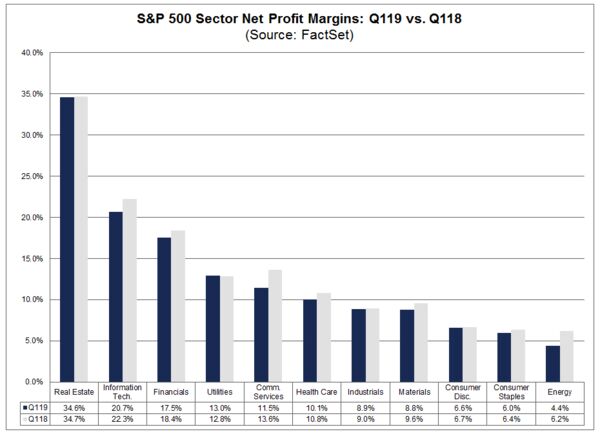

S&P 500 margins are coming in narrower than they did in the same quarter of last year, and that is the first time this has been true for some years,

Narrower margins are afflicting virtually every industrial sector.

Many companies are complaining about higher costs,

This picture could be consistent with a broad rise in labor costs eating into margins?

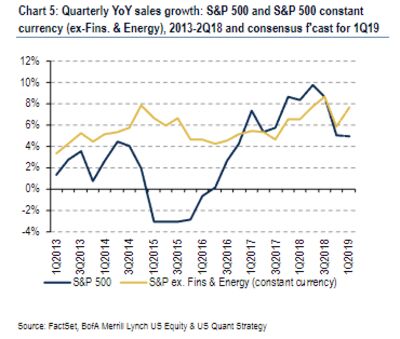

Revenues have not beaten expectations as much as they usually do but overall they still show little or no sign of a global downturn in Q1 earnings,

Where once they could not bring themselves to recommend a sell, now they cannot stomach the notion of predicting that earnings per share will go down

Bloomberg's John Authers reports:

... the numbers themselves, and the market’s reaction to them, suggest that this is a complicated and perilous environment.

Let us look at the market reception. These earnings do not appear to have been key to pushing the market to another record. Rather, companies that disappointed were strongly punished (with Google parent company Alphabet the latest and most spectacular example), while those that won the game of massaging expectations gained little reward. As this chart from the quant team at Bank of America Merrill Lynch shows, companies that missed on both their earnings and sales were punished with a 5.9 percent decline in their shares on average; those that managed a positive surprise on both measures gained only 1.7 percent:

That leads to the issue of companies’ profitability. Entering the season, the greatest concern centered on profit margins. With the labor market tightening, would we finally reach the point where margins began to shrink as employees started to grab a bigger share of the money their employers made? The answer is yes, although the full context suggests that this is still cause for great alarm.

S&P 500 margins are coming in narrower than they did in the same quarter of last year, and that is the first time this has been true for some years. But they remain wider than at any time in the three years from 2015 through 2017, as this chart from FactSet shows:

That said, FactSet also shows that narrower margins are afflicting virtually every industrial sector. Anecdotal evidence from earnings calls suggests that many companies are complaining about higher costs, and this picture would be consistent with a broad rise in labor costs eating into margins:

If that is cause for concern, there is also some positive news from sales growth, which remains healthy, particularly outside of energy and financials, which have their own issues. Revenues have not beaten expectations as much as they usually do (if we want to play the expectations game) but overall they still show little or no sign of a global downturn. This chart is from Bank of America Merrill Lynch:

Earnings season always matters to the stock market. When you buy a stock, you buy a company’s future earnings stream. But this one hasn’t resolved any of the more pressing issues currently confronting the market.

Stop me if you think you’ve heard this one before: Brokers’ analysts have still not recovered their reputation from the scandals at the turn of the last decade which revealed that they were often indistinguishable from sell-side salesmen. The way in which buy ratings outnumbered sells was always impossible to justify. That is why the game of analyzing earnings “beats” and judging companies by their performance against expectations is going out of fashion. The game, in a very real sense, is rigged.

However, in aggregate, the analysts’ estimates are not that bad. The chart below balances the Bloomberg estimated earnings for the next 12 months, compiled from analyst estimates, against actual earnings for the previous 12 months. The latter is shown with a 12-month lag. If the analysts were perfect (and nobody is), then the lines would be identical. In practice, following recommendations turns out to be a pretty good way to navigate. But still, somehow there is a light that never goes out. In one crucial respect, analysts’ institutionalized optimism remains undimmed. Where once they could not bring themselves to recommend a sell, now they cannot stomach the notion of predicting that earnings per share will go down:

There have been three earnings recessions in the last two decades. The first was driven by the fallout from the bursting of the dot-com bubble, and the second resulted from the failure of anticipating 2014’s sharp drop in oil prices. Both episodes were shallow. The hardest miss to forgive saw the analyst community utterly failing to foresee the disastrous housing crash of 2007-08 and the impact it would have on the earnings of financial companies. Analysts still fail to ask what could go wrong.

FAIR USE NOTICEThis site contains copyrighted material the use of which has not always been specifically authorized by the copyright owner. We are making such material available in our efforts to advance understanding of environmental, political, human rights, economic, democracy, scientific, and social justice issues, etc. We believe this constitutes a 'fair use' of any such copyrighted material as provided for in section 107 of the US Copyright Law. In accordance with Title 17 U.S.C. Section 107, the material on this site is distributed without profit to those who have expressed a prior interest in receiving the included information for research and educational purposes. If you wish to use copyrighted material from this site for purposes of your own that go beyond 'fair use', you must obtain permission from the copyright owner.

NOTICE Information on these pages contains forward-looking statements that involve risks and uncertainties. Markets and instruments profiled on this page are for informational purposes only and should not in any way come across as a recommendation to buy or sell in these assets. You should do your own thorough research before making any investment decisions. MATASII.com does not in any way guarantee that this information is free from mistakes, errors, or material misstatements. It also does not guarantee that this information is of a timely nature. Investing in Open Markets involves a great deal of risk, including the loss of all or a portion of your investment, as well as emotional distress. All risks, losses and costs associated with investing, including total loss of principal, are your responsibility.