ACCELERATING CREDIT LIQUIDATION WITH BOTH IG & HY SPREADS BLOWING OUT

A PUBLIC SOURCED ARTICLE FOR MATASII (SUBSCRIBERS & PUBLIC ACCESS) READERS REFERENCE

12-28-18 - "Credit Isn't Buying It: Spreads Blow Out Amid Accelerating Liquidations"

MATASII TAKEAWAYS:

MATASII TAKEAWAYS:

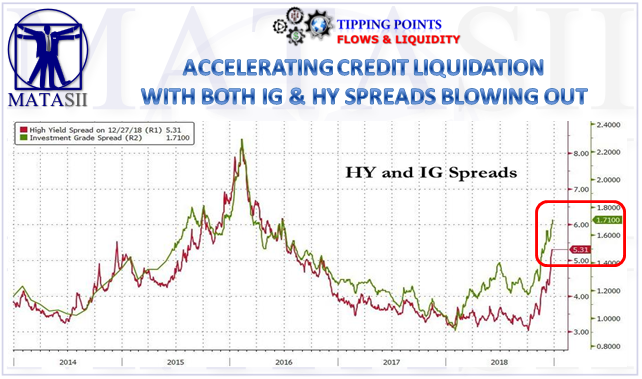

- US credit spreads, which have blown out this quarter, widened even more to the highest levels since the summer of 2016 amid accelerating credit funds outflows,

- The reason for the continued blow out is seen to be from accelerating liquidations to fund redemptions and outflows from credit funds,

- Lipper reporting that investment-grade funds saw outflows of $4.4 billion for the week ended Dec. 26, while junk bond funds registered the biggest outflows since October.

KEY MATASII OBSERVATIONS

- Unless credit spreads tighten, it will become prohibitively expensive for companies to issue bonds and fund stock buybacks in 2019,

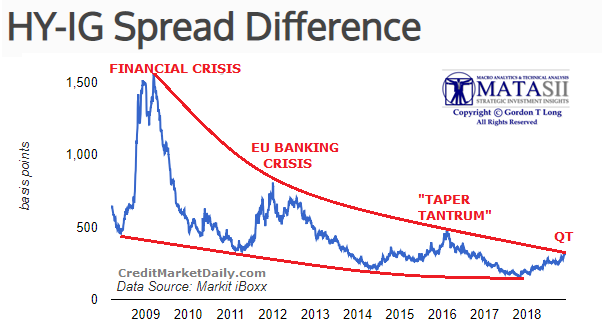

- Why have historical IG spreads (on a relative basis) moved above HY? (Suspect it has to do with highly exposed, massive build-up in BBB & expected downgrades of A, AAs).

Credit Isn't Buying It: Spreads Blow Out Amid Accelerating Liquidations

As shown below, investment-grade bond spreads widened 3 basis points to 171bps on Thursday, having widened every day since Dec. 14 and most trading sessions this quarter, confirming that the recent stock purchase has not been a universal change in moody but a stock and Treasury specific reallocation trade even as credit has continued to get pounded.

Meanwhile, junk bond also dropped on Thursday, as the high yield index widened 1 basis point to 531 basis points, the highest level since Aug. 4, 2016. It’s risen a whopping 113 basis points this month...

... with the average junk bond yield now above 8% for the first time since April 2016.

The reason for the continued blow out? accelerating liquidations to fund redemptions and outflows from credit funds, with Lipper reporting that investment-grade funds saw outflows of $4.4 billion for the week ended Dec. 26, while junk bond funds registered the biggest outflows since October.

TL/DR: someone, somewhere is buying stocks, but this is far from a universal shift in sentiment because unless credit spreads tighten, it will become prohibitively expensive for companies to issue bonds and fund stock buybacks in 2019. As a reminder, buybacks have been the single biggest source of equity demand not only in 2018 but every year since the financial crisis.