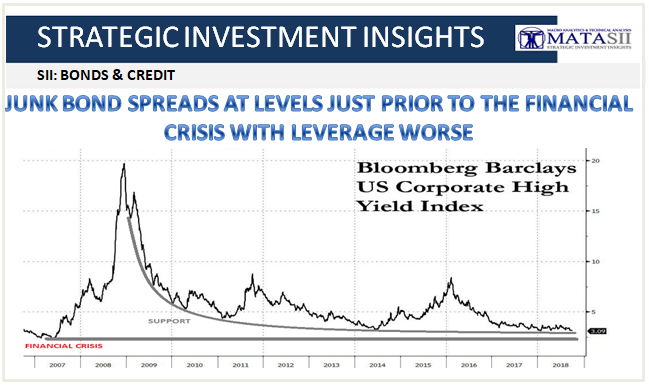

JUNK BOND SPREADS AT LEVELS JUST PRIOR TO THE FINANCIAL CRISIS WITH LEVERAGE WORSE

POST FINANCIAL CRISIS

LONGER TERM PERSPECTIVE

-- SOURCE: 10-02-18 - "Junk Bond Spreads Just Dropped To The Lowest Since 2007" --

The incredibly shrinking junk bond spread just passed a historic landmark when the Bloomberg Barclays U.S. Corporate High Yield index broke below the lowest spread since before the financial crisis this morning, dipping to 309bps, the tightest level since late 2007. This means that the extra yield over U.S. Treasuries that investors demand to own USD-denominated junk debt collapsed to the least in more than a decade.

The key reason cited by analysts has been the accelerating shrinkage in high-yield supply, as last month was the slowest September for junk bond issuance since 2011, while the high yield market as a whole has been contracting as investors have shifted their focus to leverage loans where demand, as discussed recently, has been unprecedented.

Meanwhile, fed hikes have been rising all boats, pushing debt yields across the fixed income space higher, however unlike investment grade bonds, they have a more nuanced impact on junk which is another reason why the spread has been contracting. That said, once the time comes to refinance, these issuers may feel pain as they find themselves rolling debt into notably higher interest rates. Meanwhile, thanks to the strong economy, earnings even for the distressed sector have been solid with no unexpected blow ups (think the energy sector in the aftermath of the oil recession in late 2015/early2016).

The biggest winners in the half were pharmaceutical names, but virtually every other industry group has outperformed with the obvious exception of department stores. The picture for automakers has been mixed too, although here the catalyst has been rising costs due to tariffs and confusion over Brexit: Jaguar Land Rover bonds have done worse than Tesla's, while Fiat Chrysler's have outperformed the broader index, according to Bloomberg.

The collapse in spreads has been a boon to hedge funds, with distressed debt investors generating a 6.6% return through August, outperforming the overall 0.3% gain for the broader industry and the negative total return for Investment Grade bonds.

For some of them, today's event is a sell signal: "It’s a good time to monetize," said Victor Khosla, founder of the $8.5 billion U.S. fund Strategic Value Partners LLC, which invests in distressed debt. "When high-yield spreads get to be this tight, when markets are this strong, you’re not buying as much as you’re selling."

To be sure, the collapse in spread has taken place even as overall junk bond leverage has risen to all time highs.

Others have noted that the last time spreads were this tight, the recession was about to start.

Meanwhile, for those willing to call it a day on US junk, the next big opportunities may be cropping up in emerging markets. Argentina and Brazil are among potentially promising markets as a mix of rising interest rates, currency devaluations and exiting foreign capital puts companies under pressure, according to David Tawil, co-founder and president of Maglan Capital.

Others looking for distressed opportunities will look to Asia, where widening spreads on Indonesian junk dollar bonds, accelerating defaults on Chinese corporate bonds and nonperforming loans in India suggest that there will be plenty of choices to pick from.

Not everyone is convinced that the party in US junk is over: some have said that energy names, a key component of the High Yield index, are benefiting from oil prices at 4 year highs. Others, such as Bloomberg's Sebastian Boyd, observe that there is a seasonal pattern of outperformance in the month after quarter-end leading up to results season: "If it holds, we could keep grinding tighter for another couple of weeks."

The question is just how much tighter can spreads collapse as soon return on simple cash will provide a higher return than risking capital on stressed companies that have never been more leveraged.