NOMINAL US GDP HAS FRACTURED THE LONG TERM OVERHEAD BOND MARKET YIELD RESISTANCE ZONE

-- SOURCE: 09-22-18 Lance Roberts - "Bulls Charge To All-Time Highs 09-21-18"--

...... we continue to use dips in bond prices to be buyers. This is because the biggest gains over the next 5-years will come from Treasury bonds versus stocks.

This is primarily due to the analysis, I penned yesterday on interest rates:

“While the market has been rising on stronger rates of earnings growth, due primarily to tax cuts and share buybacks, that effect will begin to roll off in the months ahead. Tariffs and higher interest costs are a direct threat to bottom line profitability, particularly when combined with higher labor costs.”

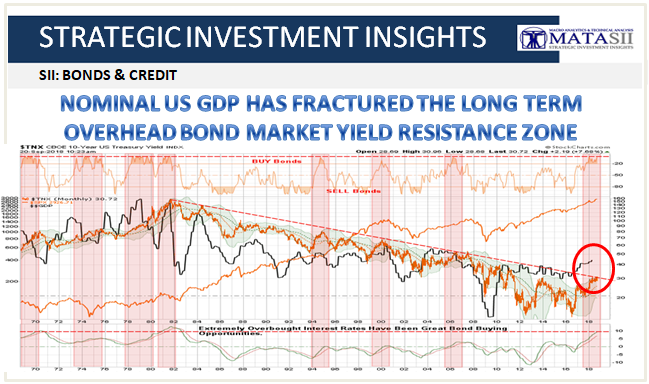

“There are several important points to note in the chart above:

- In the past 40-years, there have only been seven (7) other occasions where rates were this overbought. In each case, it was a great time to buy bonds and sell stocks. (When rates got oversold, it was time sell bonds and buy stocks.)

- There were only two (2) other periods where rates were this extended above their long-term moving averages. The one that occurred between 1980-1982 began the long-term decline in bond prices.

- Economic growth has peaked every time rates got this extended. (Which shouldn’t be a surprise.)

- Whenever rates have previously pushed 2-standard deviations of their 2-year moving average – bad things have tended to occur such as the Crash of 1974, Crash of 1987, Long-Term Capital Management, Russian Debt Default, Asian Contagion, Dot.com crash, and the Financial Crisis.”

While the markets are currently ignoring the risk of higher rates, even a cursory glance at the chart above suggests that we are near the point where “rates will matter.”

Remember, credit is the “lifeblood” of the economy and with consumer credit now at record levels, and 80% of Americans vastly undersaved, think about all the ways that higher rates impact economic activity in the economy:

1) Rising interest rates raise the debt servicing requirements which reduces future spending and productive investment.

2) Rising interest rates will immediately slow the housing market taking that small contribution to the economy away. People buy payments, not houses, and rising rates mean higher payments.

3) An increase in interest rates means higher borrowing costs which leads to lower profit margins for corporations.

4) The “stocks are cheap based on low interest rates” argument is being removed.

5) The massive derivatives and credit markets are at risk. Much of the recovery to date has been based on suppressing interest rates to spur growth.

6) As rates increase so does the variable rate interest payments on credit cards.

7) Rising defaults on debt service will negatively impact banks.

8) Many corporate share buyback plans and dividend issuances have been done through the use of cheap debt, which has led to increases corporate balance sheet leverage.

9) Corporate capital expenditures are dependent on borrowing costs. Higher borrowing costs lead to lower CapEx.

10) The deficit/GDP ratio will begin to soar as borrowing costs rise sharply. The many forecasts for lower future deficits will crumble as new forecasts begin to propel higher.

I could go on, but you get the idea.

The issue is not if, but when, the Fed hikes rates to the point that something “breaks.”

However, between now and then, the markets will likely continue to try and push higher as investor confidence continues to swell, pushing investors to take on ever increasing levels of risk, particularly as it appears as if the economy is firing on all cylinders.