RAGING ASSET INFLATION OR RISING PRICE INFLATION - ITS ALL THE SAME PROBLEM!

-- SOURCE: 12-12-17- Mises Institute - Thorstein Polleit - "Asset Prices Are Prices Too" --

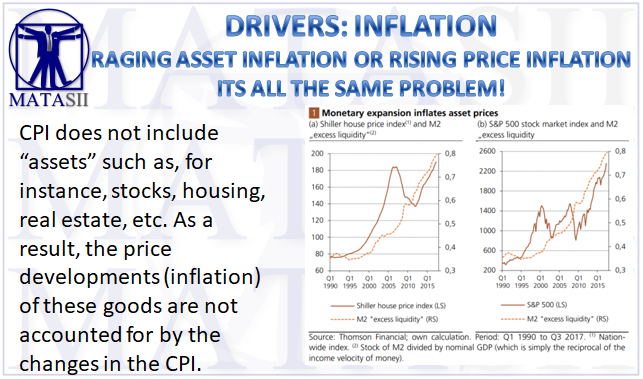

We live in inflationary times. Some people might consider this statement controversial. This is because these days inflation is widely understood as a rise in the consumer price index (CPI) of more than 2 percent per year. However, there are convincing reasons to question this viewpoint. On the one hand, the CPI does not include “assets” such as, for instance, stocks, housing, real estate, etc. As a result, the price developments of these goods are not accounted for by the changes in the CPI.

On the other hand, and even more essential, price changes of goods and services are associated with changes in the quantity of money. This is why economists used to understand a rise in the quantity of money as inflationary (and a decline in the quantity of money as deflationary): Without money sloshing around, there could not be a phenomenon like inflation — that is an ongoing upward trend in all prices of goods and services over time. The truth is that rising prices across the board is inextricably linked to money.

Asset Prices Are Prices

One indicator of an inflationary monetary development is the link between the US money stock M2 and nominal GDP. This ratio can be referred to as a measure of "excess liquidity." Since the outbreak of the crisis 2008/2009, excess liquidity has been growing strongly — as GDP growth lagged behind the increase in the quantity of money. Why? Well, a great deal of the monetary expansion has been driving asset prices upwards — most notably in the stock and housing market.

The Federal Reserve (Fed) has created yet another “inflationary boom." The US economy is fueled by extremely low interest rates, accompanied by additional credit and money growth created out of thin air. The monetary expansion leads to an artificial rise in consumption and investment spending, resulting in production and employment gains. Furthermore, the newly created liquidity finds its way into financial (asset) markets, driving up asset prices and even valuation levels.

How To Keep the Boom Going: More Inflation

To keep the inflationary boom going — and prevent the “bust,” — the Fed has to make sure that credit and money supply keep increasing and that, by no means less important, borrowing and capital costs remain at fairly low levels. That said, the ongoing inflationary policy must — and for political reasons most likely will — go on. Higher interest rates and a slowdown of credit and money creation would take away the punch bowl — and the party would come to a shrieking halt. The economic boom would turn into bust.

Inflation only works if it comes unnoticed, if there is “surprise inflation.” However, as soon as people find out that the purchasing power of money goes down more than they had expected, the chickens come home to roost: People factor in higher inflation into their contracts for wages, leases and credit. If this happens, there is no longer surprise inflation, and inflation loses its power to stimulate the economy (through misleading price signals, that is).

A central bank that wants to keep the boom going and prevent the bust is left with just one option: it has to create a higher dose of surprise inflation. The reader may already know what such an “inflation game” is leading to. It puts the economy on a high-inflation road or, in the extreme case, a super-inflation road or even a hyper-inflation road that will ultimately destroy the purchasing power of the currency.

Why There Is No Perceived Crisis

So far, financial markets have remained fairly relaxed. Inflation is not seen as a major problem as proven by, for instance, inflation expectations. How come? There might be two reasons for this. First, the majority of people derive their inflation expectations from experienced CPI inflation (we can speak of “adaptive inflation expectations”). As the latter has been relatively low for many years, people do not expect inflation to edge up in the years to come.

Second, many people still do not seem to realize that “asset price inflation” ruins the purchasing power of money in the same way as CPI inflation does: If you want to buy stocks, houses or land with your money, you will get less for your money if prices for these goods go up. However, as long as asset price inflation is not understood as a form of "true inflation," inflation expectations are tamed, and central banks can continue their inflationary scheme.

Against this backdrop we can draw two conclusions. First, inflation is alive and kicking, it is currently raging in asset price increases. Second, an inflationary boom runs the risk of turning into a bust at some point — a scenario which would hit the economy, the financial system, and asset prices hard. Unfortunately, one cannot forecast (with any scientific precision) when the boom will turn into bust; it really depends on certain conditions.

That said, the current boom may go on for quite a while — with the economies keeping expanding and asset prices rushing from one record level to the next. However, we do know from sound economics that the current inflationary boom — which is presumably welcomed by many as it provides more jobs and additional incomes — is actually sowing the seeds of a bust.

The investor should keep in mind that central banks do not only set into motion an inflationary boom in the first place (which will end in tears), but that they will fight an approaching bust with even more inflation (by increasing the quantity of money even further). That said, investors are well-advised to live up to a rather uncomfortable truth: We've had inflation, and there will be more of it. Money will continue to lose its purchasing power.