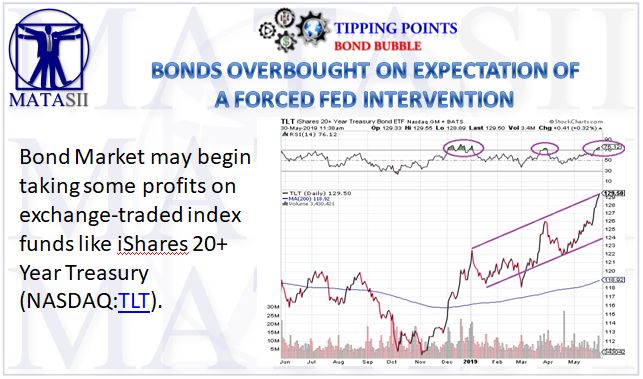

BONDS OVERBOUGHT ON EXPECTATION OF A FORCED FED INTERVENTION

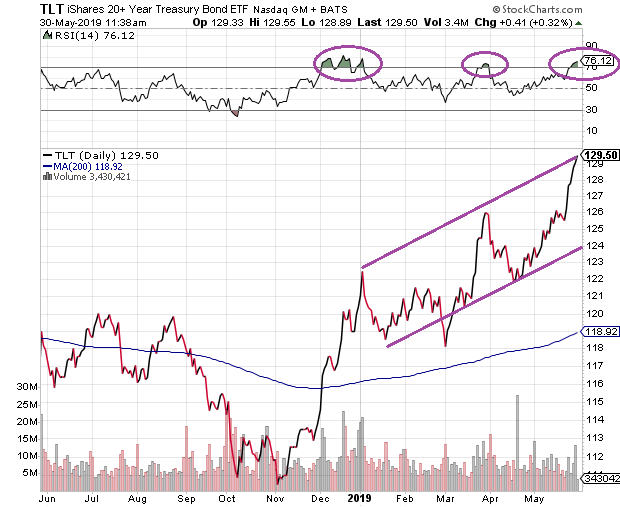

Longer-term Treasuries are overbought.

These folks may consider taking some profits on exchange-traded index funds like iShares 20+ Year Treasury (NASDAQ:TLT).

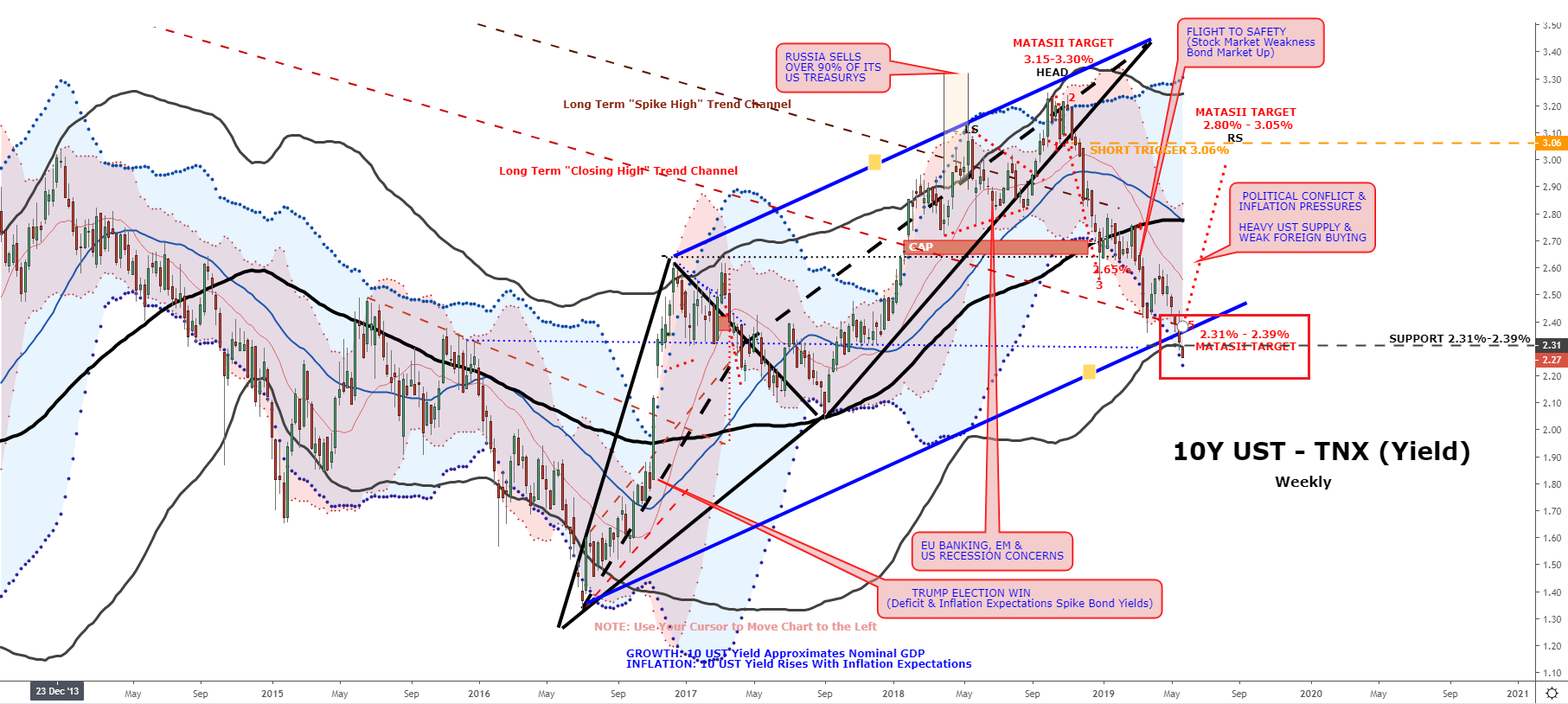

This would give us a bounce from our current support levels which we laid out earlier this week:

Below is an article by Gary Gordon of Pacific Park Financial, Inc published at Seeking Alpha which suggests the "bounce" may be little more than that but still a counter rally in falling bond yields. i.e. MATASII's "Right Shoulder".

- Why are bond market investors demanding the safety of lower-yielding, longer-term, sovereign debt? Why do many crave it more than higher-yielding, shorter-term instruments?

- Longer-term Treasuries are one of the few asset types with a bona fide track record of success in the early stages of recessions and during stock market bears.

- For active traders, longer-term Treasuries are overbought and these folks might consider taking some profits.

- For investors who may be looking to hedge their stock exposure, acquiring some longer-term Treasuries on meaningful dips can be considered.

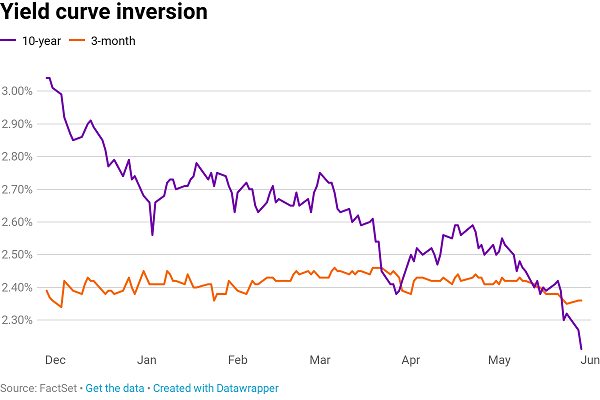

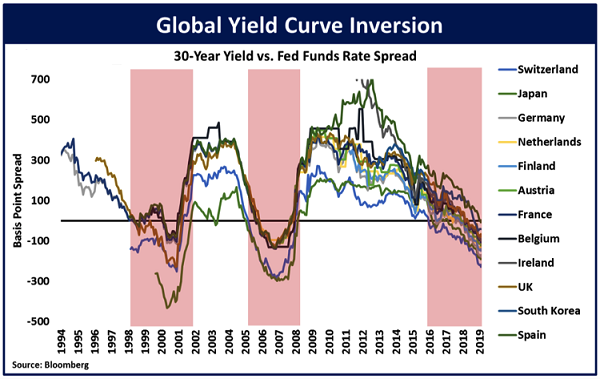

The 10-year Treasury yield pays 15 basis points less than the three-month Treasury yield. That's rather nutty when you think about it.

Even nuttier? 30-year sovereign yields across the globe are lower than the Federal Funds Rate (FFR) of 2.38%.

Why are bond market investors demanding the safety of lower-yielding, longer-term, sovereign debt? Why do many crave it more than higher-yielding, shorter-term instruments?

Investors anticipate that the Federal Reserve will need to slash its overnight lending rate in attempts to stimulate economic activity. Indeed, they have decided that the U.S. economy and the global economy are slowing considerably.

Despite the recessionary indications associated with longer-term maturities yielding less than shorter-term maturities, bullish stock enthusiasts remain unfazed. They are confident that a trade deal with China will get done. They believe that the Fed can micromanage its way through the dark with upcoming rate cuts and, inevitably, more quantitative easing.

I too believe that a trade agreement will eventually come to pass. The political stakes require a trade deal to succeed. Then again, will the trade arrangement be substantial enough to keep the global economy afloat?

I also believe that the Fed will engage in rate cutting activity soon. In fact, the central bank will ultimately resort to extraordinary levels of additional QE as well as other unconventional tools, including negative interest policy.

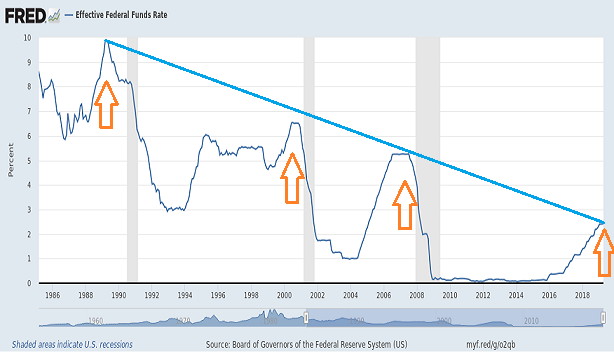

We have seen just how quickly the Fed flip-flops when asset price depreciation scares members of the Federal Reserve Open Market Committee. Three rates hikes in 2019? Nope… zero. Balance sheet reduction through 2021? Nope… it stops in September.

Yet, monkeying with interest rates and/or creating electronic money credits to buy assets (a.k.a. "QE") may not prove magical from the get-go. Previous shifts from rate neutrality to rate easing failed miserably.

Granted, the Fed can inject liquidity by electronic money printing and rate manipulation. What it cannot do is force banks to lend. Nor can the central bank force consumers or businesses to buy goods and services.

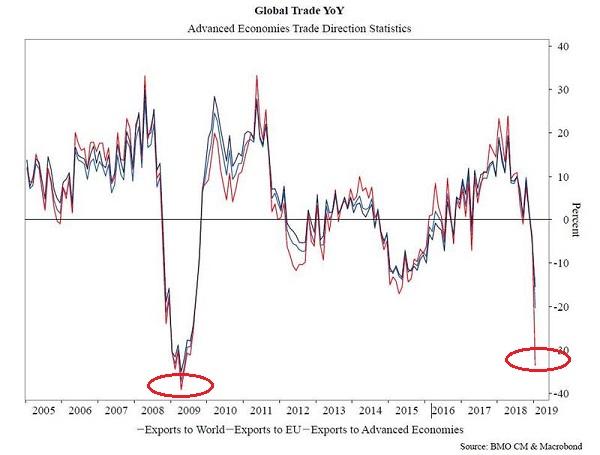

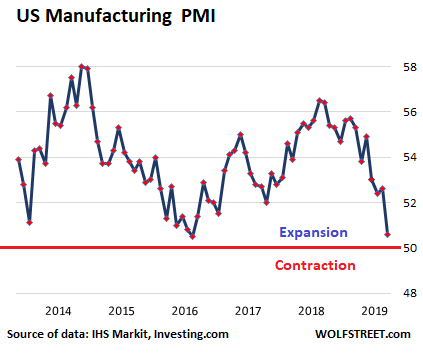

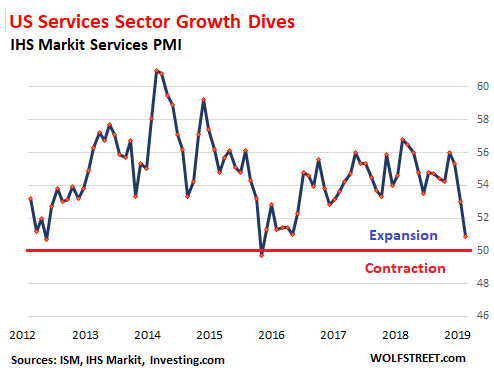

Right now, manufacturing is sickly. And consumer services do not appear to be flourishing.

It's true that the Federal Reserve successfully battled the 1998 Asian currency crisis, the 2011 sovereign debt catastrophe, as well as the 2018 quantitative tightening (QT) scare. Unfortunately, the Fed was entirely unsuccessful in stimulating the economy and reflating asset prices in either the 2000-2002 tech wreck or the 2008-2009 financial collapse.

Nevertheless, committee members are stuck with few options. If they ignore the bond market's maneuvering, asset price depreciation (e.g., stocks, fixed income, real estate, etc.) would likely result in a wealth effect reversal. People who feel significantly less wealthy stop spending. When consumers stop spending, a recession materializes.

The other option for committee members? Heed the bond market's warnings by manipulating the cost of capital downward sooner. While that may or may not give a pop to economic confidence, there's not a whole lot of room left for the future. Worse, the well-established pattern of rate suppression merely pushes a harsher recessionary reckoning further out.

One might imagine that Fed Chairman Powell and his colleagues are currently cursing their collective "bad luck." The December 2018/January 2019 pivot from rate tightening to rate neutrality appears to have purchased less than six months of equanimity.

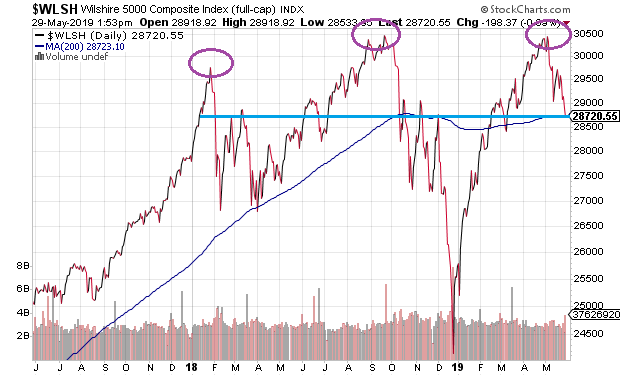

Grab a gander at the Wilshire 5000 as it battles to stay above its 200-day trend-line. Does it genuinely suggest that the bull market has done much of anything over the last 17 ½ months? Or does it seem to indicate resistance near previous tops?

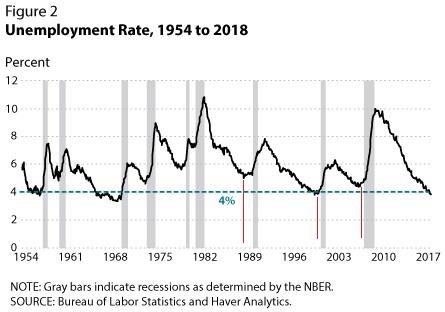

Others express that there's little reason to fret when we're sitting near full employment. Those folks do not appear to be aware of the relationship between peak employment and recessionary pressure.

Still, others confuse the current cost of capital with credit cycles. For one thing, as a cycle wanes, lenders become less willing to lend regardless of rates. Lending activity tightens.

In a similar vein, investors become less inclined to give their money to low-rung investment grade (BBB) and below-investment grade companies. Yield seeking abates. Spreads with risk-free Treasuries widen, increasing the borrowing costs for these corporations, whether it is maturing debt in need of refinancing or entirely new borrowing desires.

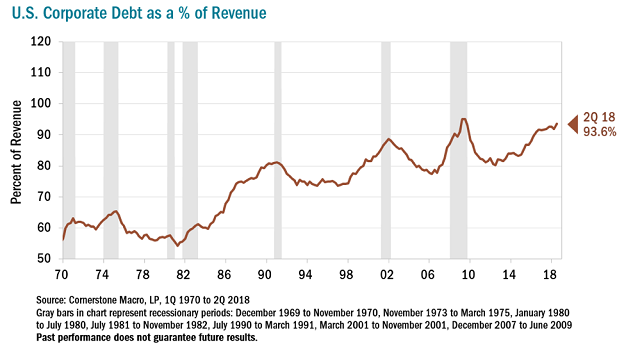

Should the credit cycle/business cycle actually contract, with corporate revenue declining and borrowing costs increasing, over-leveraged corporations discover just how difficult it is to pay what is owed, let alone operate effectively. Extremes in gross leverage, corporate-debt-to-GDP, and corporate-debt-to-revenue do not bode well.

For active traders, longer-term Treasuries are overbought. These folks may consider taking some profits on exchange-traded index funds like iShares 20+ Year Treasury (NASDAQ:TLT).

For investors who may be looking to hedge stock exposure and/or protect portfolio principal, acquiring some longer-term Treasuries on meaningful dipscould bring peace of mind. Longer-term Treasuries are one of the few asset types with a bona fide track record of success in the early stages of recessions and during stock market bears.

[SITE INDEX -- TIPPING POINTS - GLOBAL GOVERNANCE FAILURE]

A PUBLIC SOURCED ARTICLE FOR MATASII

READERS REFERENCE: (SUBSCRIBERS & PUBLIC ACCESS)

MATASII RESEARCH ANALYSIS & SYNTHESIS WAS SOURCED FROM:

SOURCE: 05-30-19 - Gary Gordon of Pacific Park Financial, Inc published at Seeking Alpha

FAIR USE NOTICE This site contains copyrighted material the use of which has not always been specifically authorized by the copyright owner. We are making such material available in our efforts to advance understanding of environmental, political, human rights, economic, democracy, scientific, and social justice issues, etc. We believe this constitutes a 'fair use' of any such copyrighted material as provided for in section 107 of the US Copyright Law. In accordance with Title 17 U.S.C. Section 107, the material on this site is distributed without profit to those who have expressed a prior interest in receiving the included information for research and educational purposes. If you wish to use copyrighted material from this site for purposes of your own that go beyond 'fair use', you must obtain permission from the copyright owner.

NOTICE Information on these pages contains forward-looking statements that involve risks and uncertainties. Markets and instruments profiled on this page are for informational purposes only and should not in any way come across as a recommendation to buy or sell in these assets. You should do your own thorough research before making any investment decisions. MATASII.com does not in any way guarantee that this information is free from mistakes, errors, or material misstatements. It also does not guarantee that this information is of a timely nature. Investing in Open Markets involves a great deal of risk, including the loss of all or a portion of your investment, as well as emotional distress. All risks, losses and costs associated with investing, including total loss of principal, are your responsibility.